While it’s tempting to place unwavering trust in data, in a world characterised by an unprecedented volume of information, low-quality data can silently undermine even the most robust decision-making processes.

Consider the direct impact: a credit decision based on flawed information can alienate customers, result in lost revenue, and incur compensatory overspending. Simply put, bad data yields wrong answers, directly impacting your portfolio's health and profitability.

Elevating your data quality for smarter decisions

The challenge lies in extracting genuine value from this vast data landscape.This involves a multi-faceted approach to ensuring the data you rely on is robust and reliable.

Data source and breadth

The depth and variety of your data sources are crucial. Limited sources or datasets lacking relevant detail often mean critical parts of the data story are missing, leading to inaccurate conclusions.

Diverse and broad data paints a clearer picture. For instance, a comprehensive commercial credit report should draw on enough data points to detail the inquirer, date, dollar value, credit type, and originating industry. When any of these fields are missing, it’s a clue that the report is probably based predominantly on ASIC search data and may lack the necessary context to interpret warning signs of credit risk.

Ensure your data provider draws on a breadth of reliable, authoritative sources spanning consumer, commercial, fraud and identity. In particular, understanding the consumer data of company directors can offer powerful insights into their overall risk profile. Additionally, understanding emerging risks such as climate risk, Environmental, Social, and Governance (ESG) requirements will necessitate incorporating new data sets into your risk assessments.

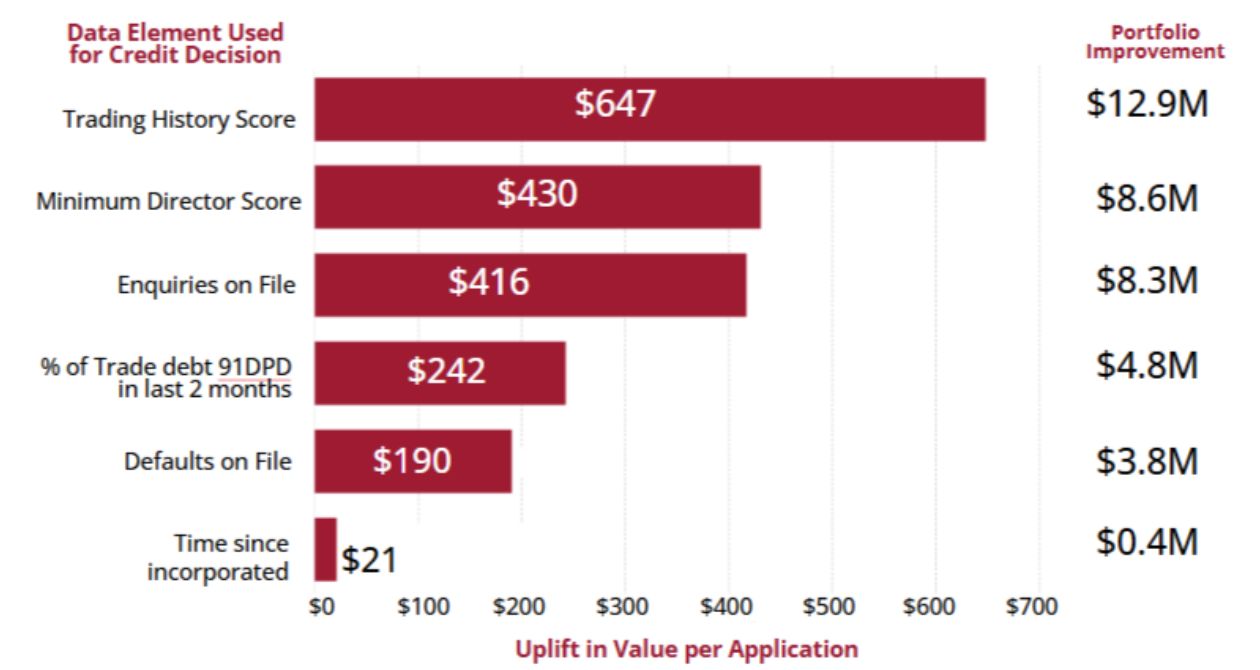

Below, an Equifax analysis of portfolio profitability demonstrates the value of quality data sources for making credit decisions.

In this hypothetical scenario, the bank processes 20,000 loan applications with an average of 8% bad rate. Bad loans cost the bank $20,000 while a good loan yields $2,000. The analysis quantifies how different data elements contribute to portfolio profitability. While individual data points like ‘Time since Incorporated’ offer some uplift, the real power lies in the synergy of comprehensive data, using a range of elements like Trading History Score (which brings in the predictive elements of the directors and enquiries on file), Minimum Director Score and Enquiries on File.

For instance, Enquiries on File can offer an uplift of $416 per application, potentially contributing $8.3M to portfolio improvement. Trading History Score (which combines all the underlying data) can potentially provide an even higher uplift of $647 per application, possibly leading to a substantial $12.9M in portfolio improvement.

This clearly demonstrates how a greater depth and breadth of data, particularly through more predictive attributes - like Trading History scores, which utilise enquiries on file, director and trade payment data - translates into enhanced profitability and more effective credit decisions for a given portfolio. Bringing all these distinct elements together through sophisticated credit risk scores provides the most effective mechanism for a predictive assessment, helping to maximise overall portfolio profitability and minimise risk.

Data freshness and real-time insights

Data can quickly become obsolete. The fresher your data, the more accurate your insights. Enquire about your data provider's refresh cadence. Real-time or near real-time data collection is crucial for identifying rapidly escalating risks. For example, unless the ASIC data your provider uses is timely and up to date, it may miss important recent credit events, thereby overlooking vital information for your risk assessment.

Equifax provides over 100M ASIC reports to customers every year. This large volume of generated reports allows us to more frequently link, match and correlate this data with our on-file data sets, constantly adding value and enriching all our credit reports.

Data matching and linkage

The ability to accurately match and link disparate data records is fundamental. A data provider's sophisticated data preparation and advanced machine learning algorithms are key to connecting various pieces of information. This enables a more complete view of financial health and customer behavior.

For comprehensive insight into a business's viability, it's crucial to connect commercial data with the consumer profiles of company directors. This holistic view can reveal critical financial instability that might otherwise go unnoticed.

As a consumer and commercial credit bureau, Equifax has the data to pull together a detailed and comprehensive profile of a director. In addition to ASIC director and shareholder information, we also link information from an individual’s consumer profile where consent is given.

Data Quality and AI-driven decisions

The rapid adoption of Artificial Intelligence (AI) capabilities further underscores the critical importance of data quality. AI models are only as effective as the data they are trained on. If the underlying data is corrupted, biased, or lacks integrity, any AI solution built upon it will produce similarly flawed outcomes.

While AI can aid in detecting and addressing some data issues, the foundational principle remains: high-quality, unbiased, and comprehensive data is essential for robust credit risk scores and effective AI-driven solutions.

Data cleansing and governance

Given the vast amounts of data businesses manage, ensuring its accuracy, reliability, and timeliness is paramount. Data cleansing, the process of fixing inaccuracies, incomplete, duplicate, or wrongly formatted records, offers significant benefits. It can prevent issues like charging deceased customer accounts, thereby reducing liability, processing costs, and improving customer service.

For credit professionals, regular data quality audits are prudent. When refreshing credit risk models, this provides an ideal opportunity for a deep dive into data integrity, leading to improved data quality and more effective risk models.

Equally important, setting up processes for the ongoing monitoring of data feeds to detect anomalies and ensure consistency. This data governance framework should include processes for refreshing data as frequently as possible, as well as maintaining the security and compliance of your data - more critical than ever as the risk of data breaches increase.

Prioritising data quality in your dealings with data providers and implementing strong internal data governance can help build a value-driven foundation to fuel the accuracy of your credit decisions.