Business Loans Rise, but SME Caution and Sectors Face Pressures in Q1 2025

The Equifax Q1 2025 Commercial Credit Report reveals a nuanced picture of the commercial credit landscape. Overall business credit applications saw a modest rise, but underlying trends reveal caution among Small and Medium Enterprises (SMEs) and significant pressures in key industries.

Key insights for Q1 2025 include:

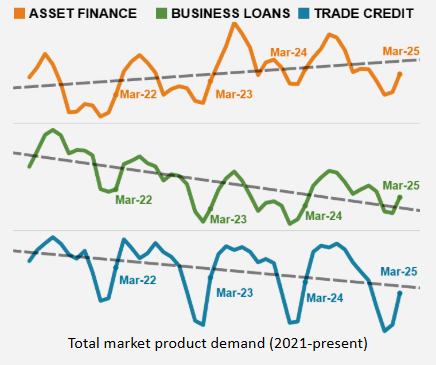

Overall demand lifted by business loans, asset finance dips

Commercial credit applications edged up by 1.6% in Q1 2025 compared to the same period the previous year. This growth was primarily fuelled by a 3.9% increase in demand for business loans, mirroring improved business confidence (which stood at 108.5 for most of Q1). It also suggests businesses are actively seeking funding, potentially for refinancing existing obligations.

By contrast, asset finance applications experienced a -2.3% decline. As asset finance is often a barometer of business confidence and willingness to make capital investments in vehicles, machinery, and equipment, this dip signals ongoing hesitancy towards longer-term expansionary projects.

Trade credit applications also softened, down -3.3%, reflecting potential slowdowns in purchasing and inventory build-up, particularly in sectors linked to consumer discretionary spending and construction.

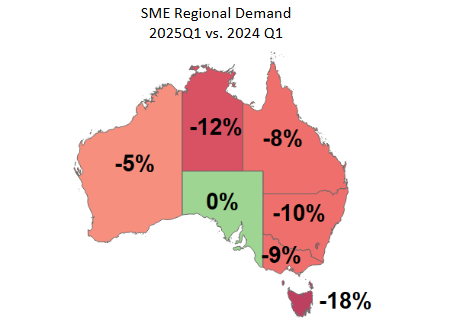

South Australia was the only state in Australia that experienced growth in overall credit demand in Q1 2025 compared to the same period the previous year, driven by increased demand for business loans and trade credit.

SMEs show restraint amid uncertainty

A significant divergence emerged between overall commercial credit appetite and SMEs. While the broader market saw a slight uptick, credit demand from SMEs in Q1 2025 fell sharply by -8.25% compared to Q1 2024. This marks a considerable drop below demand levels observed in the first quarters of previous years.

This pullback suggests SMEs are adopting a more defensive posture, likely prioritising cost-cutting and efficiency gains over productivity gains that rely on investments in technology, training, or hiring. The pressures of increased market unpredictability appear to be weighing heavily on this segment.

Credit quality of SMEs seeking finance also saw a marginal decline (average credit score change -0.51%), contrasting with the relatively stable risk profiles of larger businesses. This trend was most pronounced in the eastern states, particularly New South Wales and Victoria.

Insolvency levels continue to climb

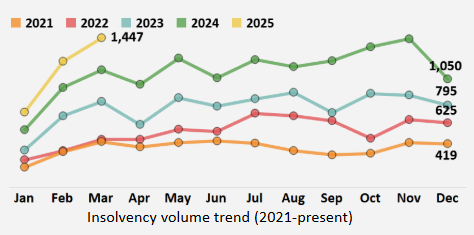

The uncertain conditions are reflected in insolvency figures. Q1 2025 saw a record of 3,393 businesses enter insolvency, a 28% jump from Q1 2024 and a dramatic 214% increase compared to Q1 2022.

New South Wales and Victoria were the primary contributors to this surge, while Queensland had the smallest insolvency increase among states. This sustained rise indicates that the economic pressures, including the withdrawal of pandemic support, are continuing to take a toll across the business community.

Construction, retail, and hospitality under pressure

Construction

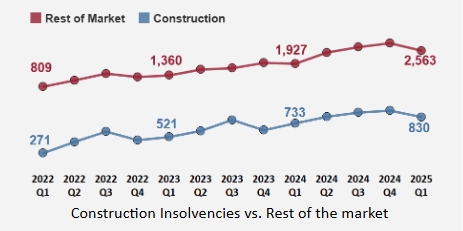

The construction sector remains a focal point of concern as it continues to exhibit the largest share of insolvencies in the market. Overall credit demand within construction fell by -10.3% in Q1 2025 compared to the same period the previous year. Although at historical high levels, there are some signs of leveling off, with insolvencies falling -11% in Q1 2025 from a peak of 929 construction companies entering insolvency in the last quarter of 2024.

Credit demand from SMEs pulled down overall demand, plummeting by -18.1%. Worryingly, there was an increase in applications from higher-risk construction SMEs, suggesting some operators may be seeking funds to stay afloat.

The construction sector also exhibits the longest trade payment delays, with construction borrowers taking approximately 2.4 times longer to pay their suppliers than businesses in other sectors.

Retail Trade

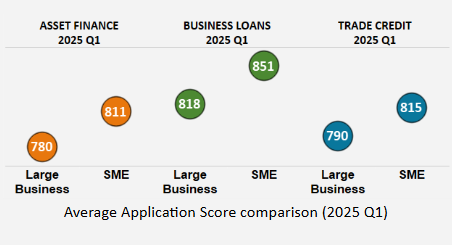

The retail sector saw overall credit demand fall by -7.4% in Q1 2025. This was largely driven by a -10.1% contraction in demand from larger retail businesses. SMEs in retail showed a smaller drop in demand (-4.2%), perhaps indicating a greater need to access credit for ongoing operational funding.

An interesting counterpoint is that SME applicants in retail generally presented with higher average credit scores than their larger counterparts, especially for business loans and asset finance products.

While retail insolvencies rose 24% year-on-year, the levels have stabilised over the last three quarters, having reached peak levels in the second quarter of 2024.

Retailers are also demonstrating better trade payment performance, consistently repaying debt faster than other sectors. Their average repayment time has improved by nearly a half a day since its peak in Q4 2023.

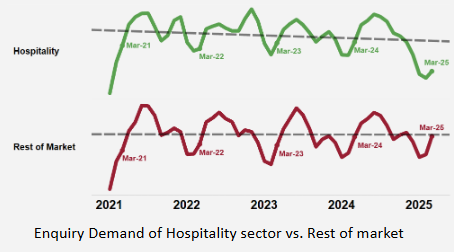

Hospitality

The hospitality sector experienced the most severe downturn in credit demand, falling by -16.9% in Q1 2025. Similar to retail, larger businesses in hospitality cut back credit seeking more sharply (-25.2%) than SMEs (-10.2%).

While overall customer quality for the sector remained stable compared to Q1 2024, SMEs tend to have significantly higher credit scores than large businesses, particularly those SMEs applying for business loans and asset finance

Insolvencies in hospitality were up 32% compared to Q1 2024, though current levels have reduced -25% from the peak seen in Q4 2023. This sector is highly sensitive to inflation and consumer discretionary spending, which has been eroded by cost-of-living pressures. 56% of Australians in an Equifax survey reported cooking at home more to save on dining out.

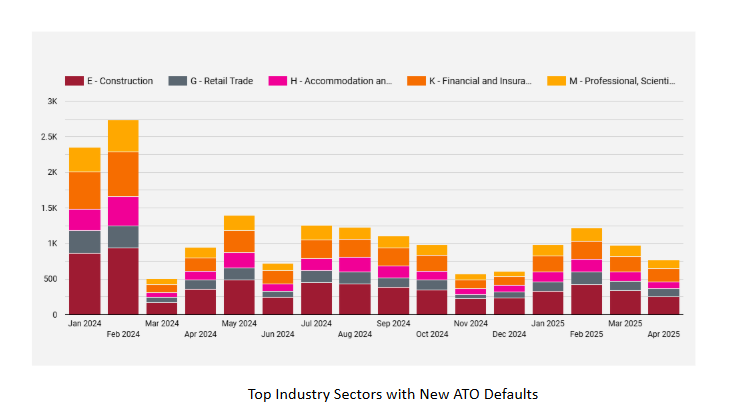

Consider high ATO defaults as part of a broader picture

The volume of active Australian Taxation Office (ATO) defaults remains elevated, with approximately 30,320 entities having an active ATO default in Q1 2025, totalling around $9.48 billion (an average of $410k per default).

While the rate of new ATO default listings has stabilised in Q1 2025 (about 60% of levels seen last year), the overall number indicates significant ongoing financial stress for many businesses.

Construction accounts for the highest proportion of new ATO defaults at 22% in Q1 2025, followed by Financial Services (14%), Accommodation & Food Services (9%), and Retail Trade (9%).

While an ATO default is a clear indicator of financial difficulty, analysis suggests its predictive power for external administration is similar to that of other financial defaults. Therefore, credit professionals should view ATO defaults as an important risk signal but within the context of a comprehensive credit assessment that includes broader financial defaults.

How to make better credit decisions in a complex market

The Q1 2025 commercial credit data underscores a complex operating environment with sector-specific risks and differing credit risks of SMEs versus larger enterprises. As Australia’s leading consumer and commercial credit bureau, Equifax provides a comprehensive and consistent view of potential risk through its extensive data sources, credit reports, and alerts.

Equifax has the unique capability to combine individual and business financial information into a single comprehensive credit report, allowing credit professionals to gain a more holistic view of an applicant’s financial health.

By leveraging advanced AI scoring models and precise data linking technologies, Equifax improves the accuracy of risk evaluation for more informed and confident lending decisions.