Small-scale operators in Australia’s construction industry could well be the canary in the coal mine for the difficulties that lie ahead for this sector. Rising rates of construction industry insolvencies and cost of living pressures continue to place a heavy financial burden on sole traders and small business owners, who make up 97%1 of construction companies.

The significant increase in construction company failures since the start of the year shows no sign of abating. Provisional data indicates that construction insolvencies increased 19% for the month of May, sitting 43% higher than last year (May ‘21).

While construction insolvencies have increased 30% over the last twelve months, the more recent increase in company collapses can be attributed to the mounting pressures of disrupted supply chains, rising material costs, labour constraints, inclement weather and project delays. Construction insolvencies across the months of April and May were 47% and 43% higher, respectively, than last year.

Compounding difficulties are additional stressors like inflation, the rising interest rate environment, increased insurance costs and renewed debt recovery efforts from the Australian Taxation Office (ATO). Higher interest rates contribute to higher borrowing costs and, together with increasing presales requirements and reduced interest cover, the industry will face increased refinance risks and associated funding constraints. During a period of project delays, these market factors have collectively contributed to operating cash flow constraints and liquidity risks, especially for the many construction firms that are thinly capitalised with limited borrowing capacity.

Insolvency data warns of hard times ahead

The total number of construction and non-construction companies entering external administration in Australia in May was more than 30% higher than last year, notably across the Eastern seaboard. Particularly noticeable is the substantial increase in creditor wind-ups, voluntary administrations and restructuring appointments. Creditor wind-ups have triggered the majority of insolvencies, and the construction sector has grown to represent 28% of all Australia-wide insolvencies.

Equifax, through its credit ratings agency2, conducts a large number of detailed credit ratings engagements across the construction industry each year, typically scrutinising the financial statements of medium and larger-sized construction companies. Equifax’s ratings business has observed a deterioration in credit ratings at the lower credit quality end of these companies, highlighting risk across both large and small construction firms.

This deterioration is particularly concerning given the widespread use of integrated project delivery in the construction sector, where several parties work together to optimise results. This cascaded delivery model escalates the contagion risk, creating a house of cards where a single failure of a head contractor can have catastrophic consequences for other parties in the broader delivery chain.

The challenges for construction companies are widespread, and the collapse of major firms like Probuild and Condev illustrates that long-standing businesses are not immune. In the quarter ended March 2022, nearly half (47%) of all construction businesses that went into external administration had been trading for ten or more years.

Small operators under pressure

It is not just the larger operators under strain, with small construction businesses increasingly finding it difficult to cope with the growing slew of pressures.

Interestingly, only 8% of small businesses (more broadly) sought additional funds over the past three months; however, a review of the information about why the large majority had not sought funds provided some valuable insights. While half (49%) reported they were unwilling to increase their debt levels, 6% were unable to meet their debt repayments, and 5% were unable to meet the eligibility requirements3.

Typically, many smaller operators support their businesses through personal loans, using assets like their family home as collateral. In its role as the largest consumer and commercial bureau in Australia, Equifax has an unparalleled ability to assess the credit risk of both businesses and the people behind them. Equifax data shows that smaller operators may be dipping into their personal finances to keep their operations afloat.

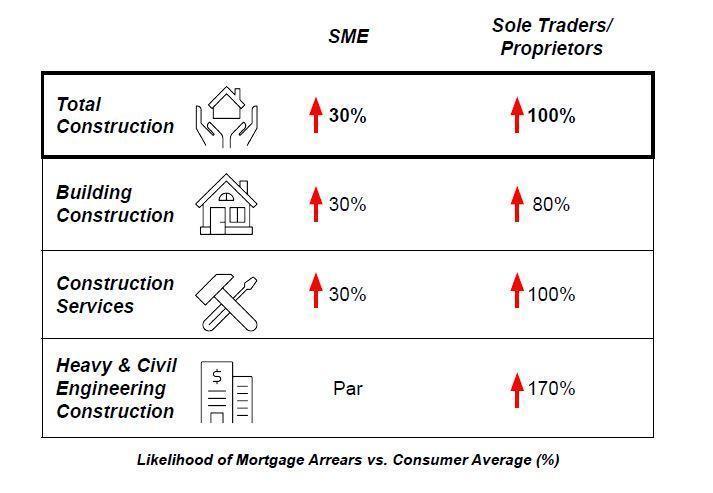

Most (97%) of the 410,850 construction businesses in Australia (June 2021) are small businesses, earning less than $5M in annual sales revenue. Equifax data shows the mortgage arrears rate for construction industry sole traders has been trending up since November 2021 and is now twice that of the average consumer.

Brad Walters, Head of Product and Ratings Services at Equifax, said: “Small businesses are the engine room of our economy, and people are increasingly looking beyond the tip of the iceberg to understand what is happening below the surface".

Specifically, proprietors of building construction businesses are 80% more likely, and directors of building construction companies are 30% more likely, to have missed mortgage repayments than the average consumer.

Director Penalty Notices

The ATO has resumed its debt recovery activities put on hold during the pandemic. This includes issuing Director Penalty Notices (DPNs), which hold directors personally liable for the tax debts of their business. The outstanding tax debts that companies have been able to accrue on their balance sheets must now be paid, further exacerbating stress across the sector.

More recently, as a part of this process, the Government is sharing with Equifax (as a credit reporting bureau) the identity of those parties with a significant tax debt that have not otherwise engaged with the ATO on a tax payment plan. This further increases transparency and, when combined with the growing number of DPNs, will likely see more companies put into administration/liquidation.

Margin Erosion

Rising costs, disrupted supply chains and periodic lockdowns have created what many refer to as a ‘profitless boom’, where construction companies are committed to fixed-price projects that may no longer be financially tenable given the major price increases for building materials.

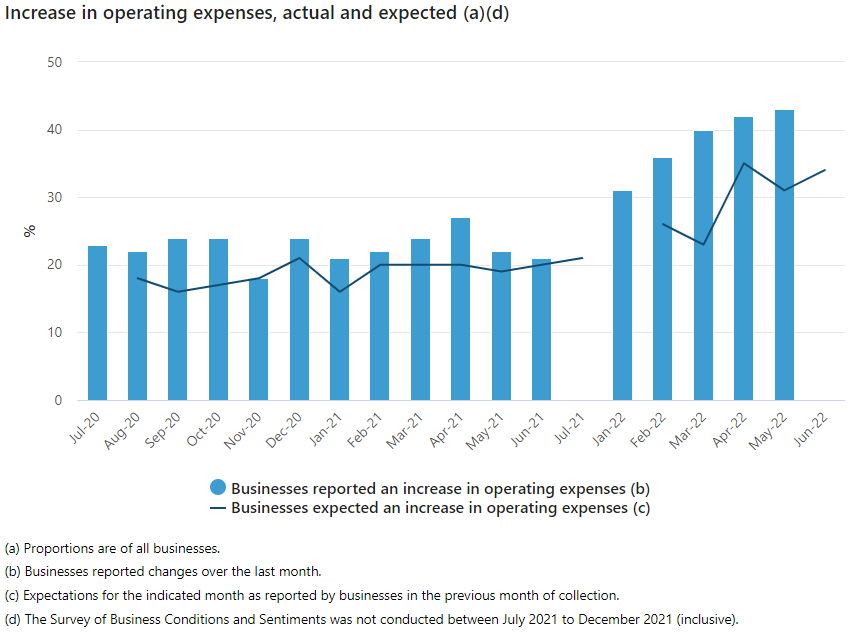

Operating expenses remain elevated, with businesses reporting cost increases double last year’s increases. Figures just published by the ABS for June 2022 show that nearly half (46%) of Australian businesses experienced increased costs over the prior month, compared to only 21%4 for June of the previous year. Of these businesses, 52%5 have not passed on these increased costs, further eroding profit margins. When considering the month ahead, 44% of companies expect operating expenses to grow, the highest recorded since the ABS first asked this survey question in July 2020.

More specifically, the costs of building a new home have increased by 15% over the last twelve months, and are anticipated to continue rising in the months ahead6. These cost escalations are particularly problematic for smaller and/or more thinly capitalised operators, constrained by fixed-price contracts from passing on costs to consumers. Their ability to contractually renegotiate is limited without rise and fall clauses or other contingencies. As the work drags over many months and the costs of materials and operating expenses go up, completing the project to budget becomes increasingly challenging.

This pressure is exacerbated by increased build times, which have expanded from an average of 8 months to complete, to now more than a year7. Some operators find themselves having previously signed onto contracts that they must continue to progress for months to come, knowing they are trading at a loss. This is a dangerous position to be in as many businesses are cash flow dependent and already operating on thin margins.

Even large operators seeking to renegotiate their contracts with customers may find they are constrained by the threat of consumer backlash and reputational damage. Last year business exit rates were double the entry rates for construction businesses with more than $5M annual sales.

Compounding the problem is the escalation in the cost of materials due to supply chain constraints. The ABS reports that more than two in five businesses (41%) are experiencing supply chain disruptions in June 2022. This figure has remained steady since it peaked in January 2022 at 47%. With global supply chains thrown into disarray from COVID and the war in Ukraine, there’s upward price pressure on materials during elevated domestic building demand where significant rebuilding efforts are required in flood-impacted regions. A little over a year ago, in April 2021, only 30% of businesses reported supply chain disruptions.

Add to these challenges are the knock-on effects of constrained resources, labour shortages and COVID sick days that have contributed to project delays. In June 2022, the ABS reports that almost a third (31%) of employing businesses, including construction firms, are having difficulty finding suitable staff. Of these, small and medium companies are much more likely than large companies to experience a substantial flow-on impact on their operations. The most common factors businesses cited for a staff shortage include lack of job applicants (79%) and applicants not having the relevant experience and qualifications (59%).

Insurance challenges

Maintaining sufficient insurance cover is difficult in this harsh trading environment. APRA data shows that gross construction claims have previously trended higher than gross earned insurance premiums for property-focused insurance. In 2020, the gross loss ratio (GLR) for property-focused insurance performance was 104% nationally, before considering additional costs such as acquisition and operating expenses.

Considering that insurance premiums represent the cost of risk, this unsustainable equation has understandably seen a rise in premiums. With insolvencies trending upward and numerous government reports highlighting the prevalence of construction defects, the construction industry has taken on a higher risk profile.

Unfortunately, these construction woes come at a time when Australia’s housing shortfall dictates a need to build more, not less. Without the capital, resources, labour, materials and the supply, it looks to be an uphill battle that will only worsen as our borders open once more to immigration.

Encouraging trustworthy players

Despite the real challenges the construction industry faces, Mr Walters said, “It’s not all doom and gloom. There are still operators exhibiting sufficient financial capacity, capital, capability and resilience to weather the storm.”

To recognise and reward these trustworthy players, the NSW Government has facilitated a market-led ratings regime. Construction businesses now have the opportunity to go through an independent and rigorous review process to obtain a star-rating outcome that substantiates and rates their reliability and resilience.

The new Independent Construction Industry Rating Tool, iCIRT from Equifax*, shines a light on the trustworthy players who are seeking to differentiate themselves from unscrupulous and high-risk operators. This improved transparency works toward developing public trust and is one of the critical pillars of the NSW Government’s reform strategy for the building industry.

Constructors rarely collapse overnight, so data-driven star-rating insights can be used as an early warning tool to cut through where risk sits across the construction ecosystem. The demise of Probuild is one of many examples of constructors that have been exhibiting an increasing risk profile over the last few years. This infographic, Red Flags to Probuild Collapse, demonstrates the trouble it was in years before it plunged into administration. Data points used within iCIRT showed its risk rating deteriorating from 2.5 bronze stars in 2019 down to only 1 bronze star in 2021.

Calling all developers to get rated

Last month saw the release of the first tranche of developers and builders rated as trustworthy through iCIRT. For the first time in Australia, those seeking to purchase a home or an apartment have a register they can search to find developers and builders with a proven track record of quality and integrity, supported by objective evidence of their past capability.

Construction professionals are being encouraged to undergo an independent, rigorous review process to obtain a rating of between one and five stars. The more stars, the more confidence the public can have that the construction firm, design practitioner, consultant and/or certifier is likely to deliver a more reliable outcome. Only parties with three or more gold stars are included on the iCIRT register.

“iCIRT brings much-needed visibility to an industry where reliable, objective data has up until now been hard to come by,” said Mr Walters.

“It takes away the guesswork of deciding which builders or developers to engage with, by applying an independent, holistic and evidence-based assessment. A quick search of the register shows those who have met the eligibility criteria to be recognised as trustworthy providers and have agreed to publish their star rating.

“Importantly, iCIRT will help protect people from physical, emotional, and financial harm, leaving those few industry players that have been doing the wrong thing with nowhere to hide, while providing a fair and equitable playing field for those doing the right thing. Helping people live their financial best is at the heart of our purpose at Equifax.”

Good news for insurers and industry on risk

Insurers are among many stakeholders looking for improved transparency to restore trust. Given the elevated risks of construction insolvencies, it’s no surprise we’ve seen a growing demand for rating insights to strengthen insurer appetite in this market. This is especially relevant as global reinsurers have sought to deploy their capital in segments and jurisdictions viewed with more favourable risk-return fundamentals.

To this end, ratings have been recognised as being critical in strengthening transparency and confidence, with insurance premiums based on underlying risk profiles rather than competitive market factors. As one example, SIRA recently amended its guidelines to enable insurers to adopt rating tools provided by regulated rating businesses for both eligibility and premium purposes.

Equally, they have been embraced by an industry seeking improved transparency and the recognition of reliable and resilient constructors. With the growing number of construction insolvencies, risk and credit managers will benefit from leveraging ratings insights across this segment.

* iCIRT by Equifax is an independent construction industry star-rating tool to assess building professionals. Equifax, a global data, analytics and technology company, provides the iCIRT service through its subsidiary business Equifax Australasia Credit Ratings Pty Ltd, which is a regulated ratings agency with the required rigour, discipline and oversight to ensure rating outcome integrity and independence. Our large number of existing market connections and significant data assets enable us to lift the corporate veil and provide confidence to the market by leveraging digital insights from over 900 million consumers and businesses across 24 countries.

This article was first published in abridged form in the AICM Risk Report.

1 Small businesses – those generating <$5m in sales revenue – represent 97% of the 411k construction businesses in Australia as at June 2021

2 Equifax Australasia Credit Ratings Pty Ltd holds an Australian Financial Services License to provide credit ratings to wholesale clients [AFSL#341391]

3 Note: Businesses could provide more than one response on why they were not seeking additional funds. Source: https://www.abs.gov.au/statistics/economy/business-indicators/business-c...

4 Business Conditions and Sentiments, June 2022, https:// www.abs.gov.au/statistics/economy/business-indicators/ business-conditions-and-sentiments/latest-release

5 Business Conditions and Sentiments, April 2022

6 https://www.theaustralian.com.au/nation/politics/home-build-cost-crunch-...

7 https://www.theage.com.au/national/victoria/new-home-build-times-blow-ou...

Related Posts

Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.

Equifax can now share data via Snowflake Marketplace, giving brands and businesses access to fast and secure data sets including Australian consumer credit trends, consumer and commercial data.