Consumer credit demand set to shake off lingering impacts of COVID

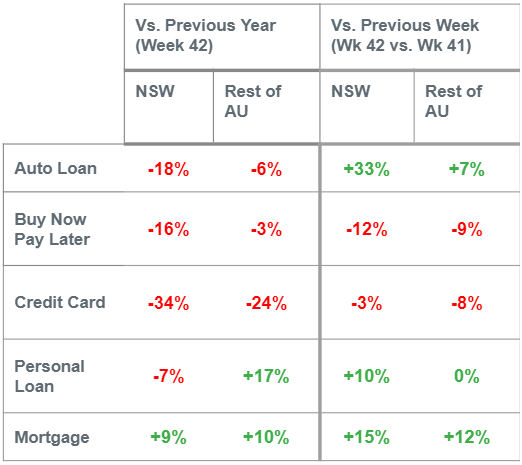

Consumer credit demand continues its upward trajectory in Q3 2021, with early indications of further recovery in the coming months. Data from the first week of NSW reopening after 15-weeks in lockdown shows a jump in demand for auto loans (+33.0%), mortgages (+15.0%) and personal loans (+10.0%) compared to the previous week in lockdown.

Equifax Quarterly Consumer Credit Demand Index: Sept 2021

-

Overall consumer credit applications increased by +12.8% (vs Sept quarter 2020)

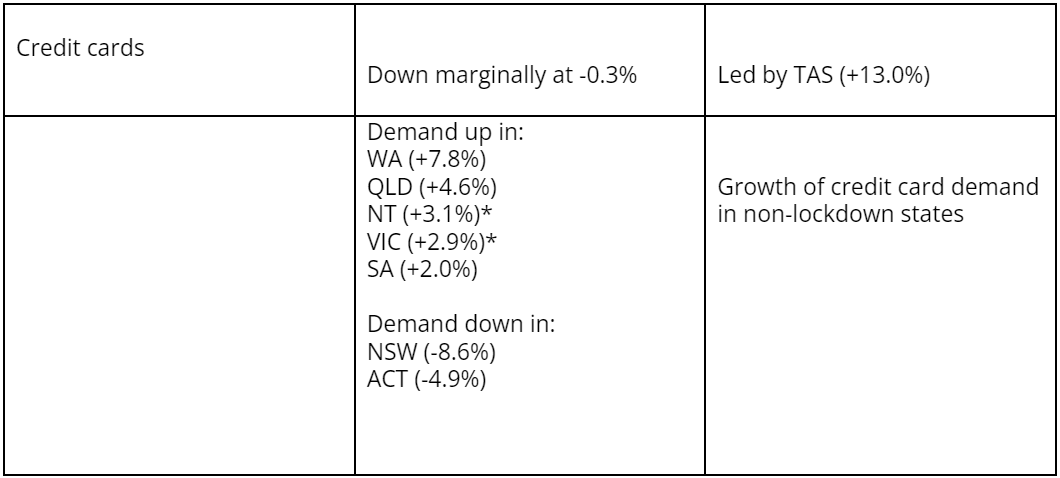

- Credit card applications flat -0.3% (vs Sept quarter 2020)

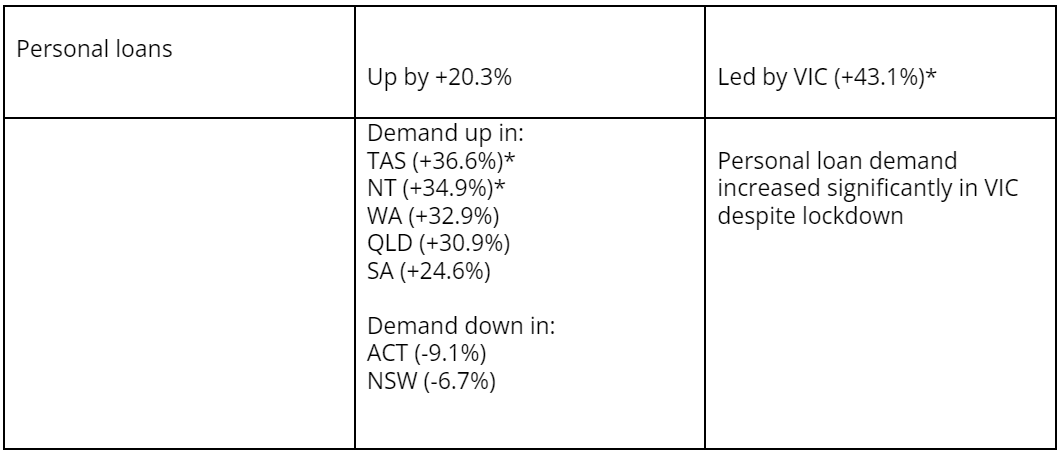

- Personal loan applications up +20.3% (vs Sept quarter 2020)

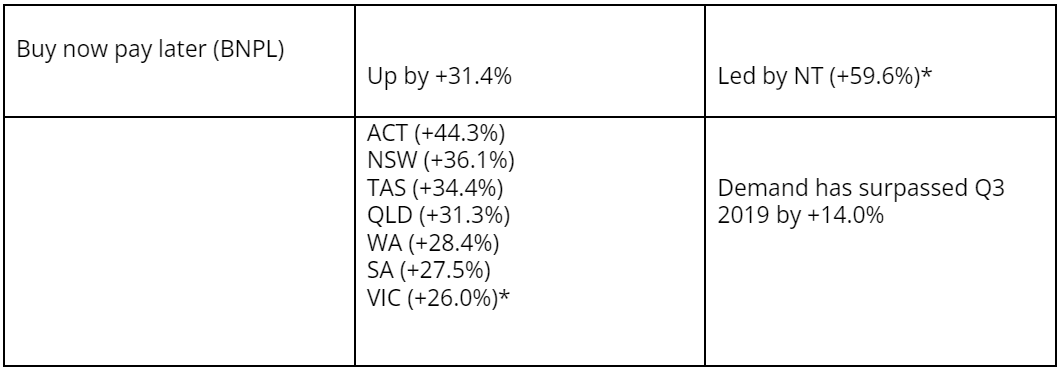

- Buy now pay later applications grew +31.4% (vs Sept quarter 2020)

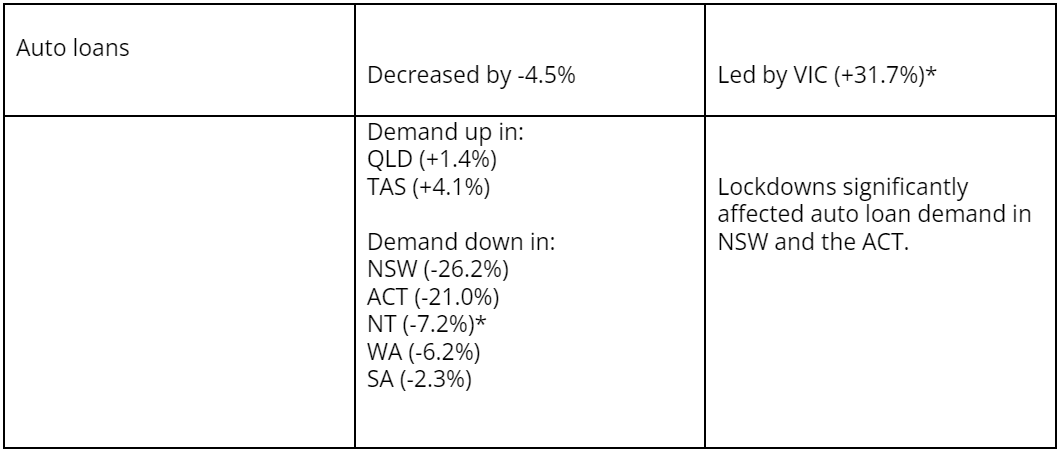

- Auto loan applications reduced by -4.5% (vs Sept quarter 2020)

- Mortgage applications up +13.1% (vs Sept quarter 2020).

SYDNEY – 26 October 2021 – Consumer credit demand continues its upward trajectory in Q3 2021, with early indications of further recovery in the coming months. Data from the first week of NSW reopening after 15-weeks in lockdown shows a jump in demand for auto loans (+33.0%), mortgages (+15.0%) and personal loans (+10.0%) compared to the previous week in lockdown – refer to image 1.

The prospect of a bounce-back once NSW and Victoria ease their lockdown restrictions is supported by indicators from the latest Equifax Quarterly Consumer Credit Demand Index (Sept 2021). Released today by Equifax, the global data, analytics and technology company and the leading provider of credit information and analysis in Australia and New Zealand, the index measures the volume of credit applications for credit cards, personal loans, buy now pay later (BNPL) and auto loans.

Kevin James, General Manager Advisory and Solutions, Equifax, said: “With international travel soon to reopen, we can expect to see consumer credit demand grow, specifically the use of credit cards to pay for people’s overseas holidays.”

“It should also hasten Australia’s economic recovery that we’re moving into a quarter that traditionally sees higher spending with Christmas approaching.”

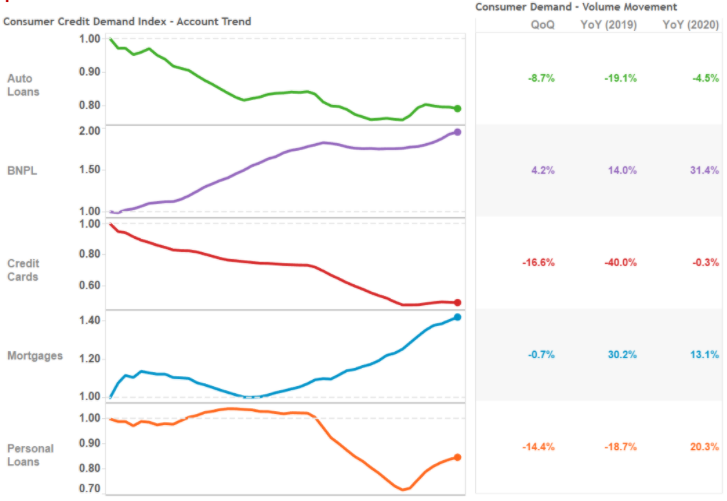

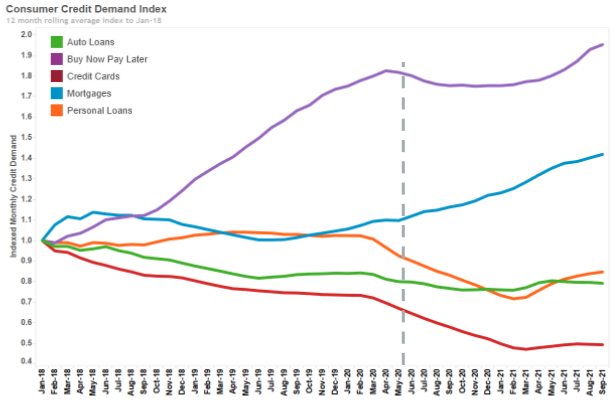

Overall, consumer credit applications were up +12.8% in the September 2021 quarter compared to the same quarter in 2020. This uptick was driven by the strong performance of BNPL, mortgage and personal loan applications. Demand for mortgages and BNPL has surpassed pre-COVID levels, with mortgage enquiries up by +30.2% and BNPL +14.0% compared to Q3 2019 – refer to image 2.

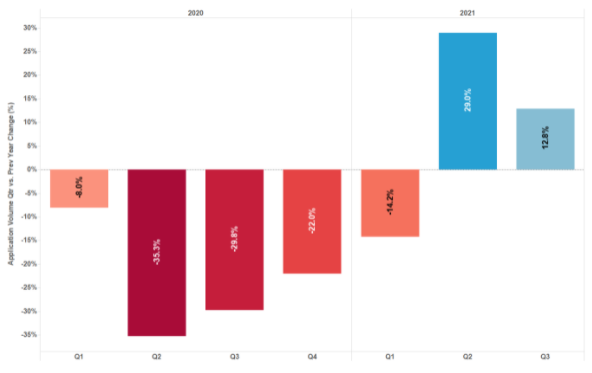

Despite these gains, overall consumer credit demand remains -20.8% lower than its pre-COVID level (Q3 2019).

“Mortgage and BNPL demand have remained strong in and out of lockdowns, but their gains haven’t been enough to offset the drop in other categories of credit. Now that Australia is reopening, we can expect to see credit cards, auto loans and personal loans playing catch up,” said James.

While data from NSW’s first week out of lockdown shows a decline in BNPL demand (-12%), it is expected this will be a temporary dip as consumers settle back to in-store shopping.

Auto loan demand reduced by -4.5% in the September 2021 quarter compared to the same period in 2020, but this was not uniform across Australia. The locked-down states of Victoria, NSW and the ACT were trending down in auto enquiries when compared to their pre-COVID levels.

Now that restrictions are easing, auto loan enquiries are likely to turn around in the locked-down states as the demand for vehicles normalises. During the first week out of lockdown in NSW, auto loan enquiries rose by +33.0%.

Personal loan demand surged by +20.3% in the September 2021 quarter compared to the previous year, with enquiries nearly approaching the pre-pandemic level. NSW and the ACT were the only two jurisdictions not to share in this uptick, but data from the first week of NSW reopening shows positive signs that personal loan demand will recover as lockdowns end.

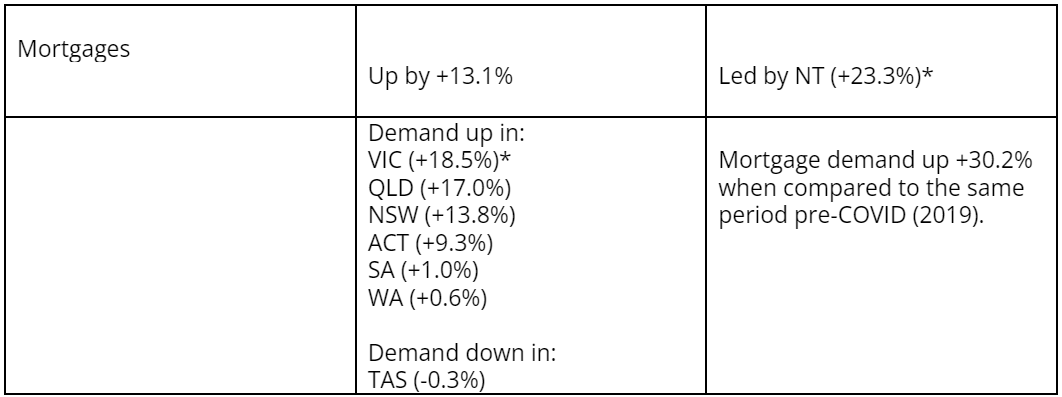

TABLE 1: Consumer Credit Demand by State (VS Same quarter 2020)

Mortgage Demand

* Victoria was in lockdown for the majority of the September 2020 quarter

*Low volumes

IMAGE 1: Consumer Credit Demand for NSW and the rest of Australia for the week for the 1st week that lockdown restrictions ease in NSW (11-16 October 2021)

IMAGE 2: Consumer Credit Applications – Indexed by Type and Volume Movement

IMAGE 3: Consumer Macro Credit Demand – Quarterly YOY

IMAGE 4: Consumer Credit Applications – Indexed by Type

* The data has been re-indexed* from 2018 to account for the recent inclusion of Buy Now Pay Later applications:

Re-indexed data to commence in 2018 (previously 2015)

Added buy now pay later and auto loan credit enquiries as a separate trendline (previously rolled up into personal loans)

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employees, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by more than 11,000 employees worldwide, Equifax operates or has investments in 25 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

[email protected]

NOTE TO EDITORS

The Quarterly Consumer Credit Demand Index by Equifax measures the volume of credit card, personal loan, applications, Buy Now Pay Later and auto loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Key highlights:

KYC now requires a broader approach, blending identity data with behavioural data to identify risk patterns. Criminals are using complex corporate ownership structures to hide behind, making interconnected commercial data critical for KYB. Successful KYP needs to blend the technology of regular screening with interpersonal conversations to help detect risk.

Q2 2026 analysis by Equifax Australia into consumer credit trends highlights how households are navigating ever changing economic conditions.