Consumer credit demand soft but rate of decline slowing

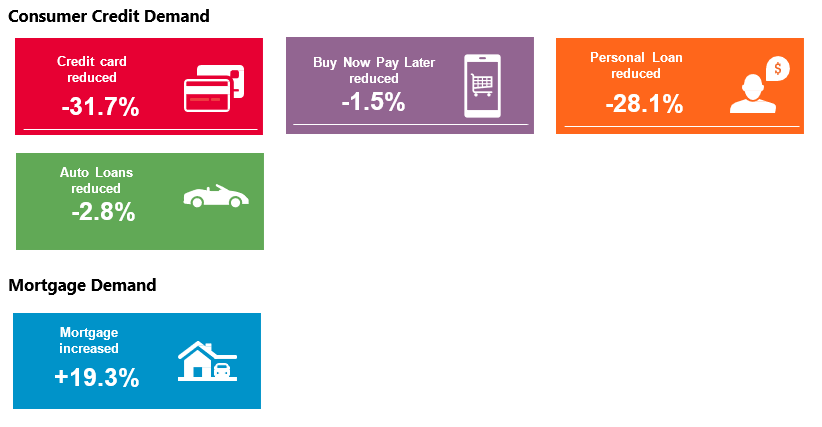

Overall consumer credit applications down -21.9% (vs December quarter 2019)

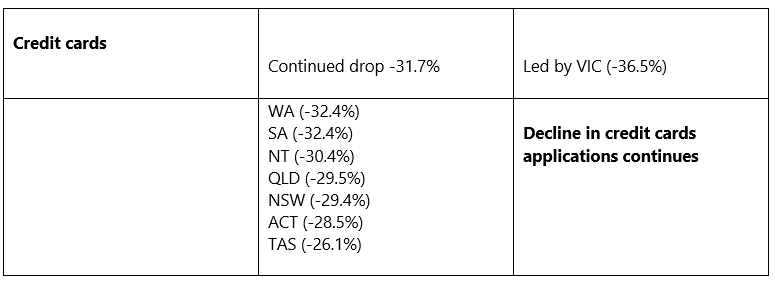

- Credit card applications reduced by -31.7% (vs December quarter 2019)

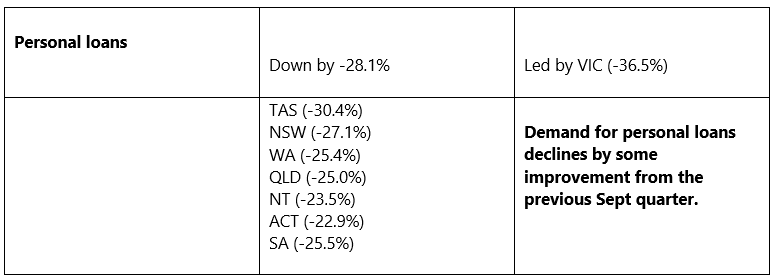

- Personal loan applications dropped -28.1% (vs December quarter 2019)

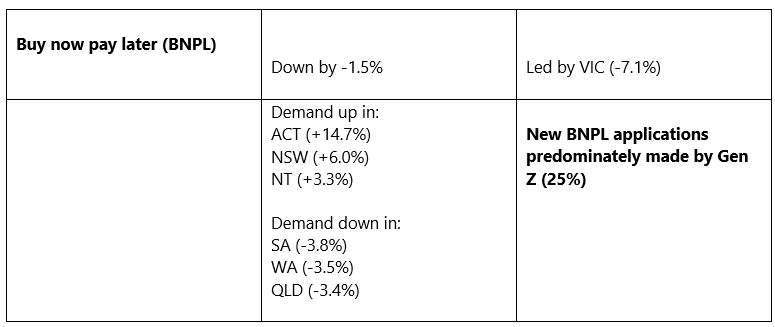

- Buy now pay later applications trending down -1.5% (vs December quarter 2019)

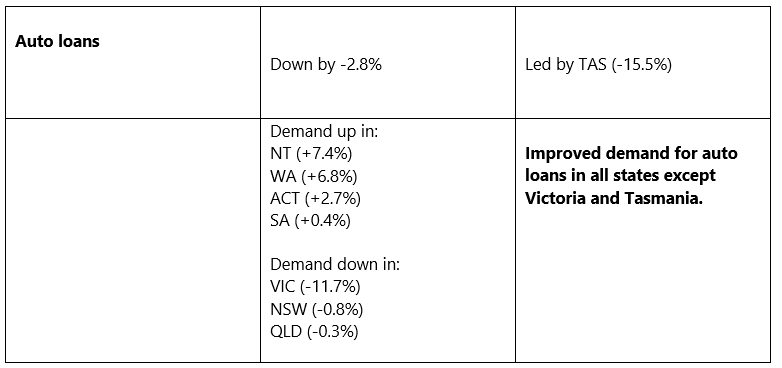

- Auto loan applications decreased by -2.8% (vs December quarter 2019)

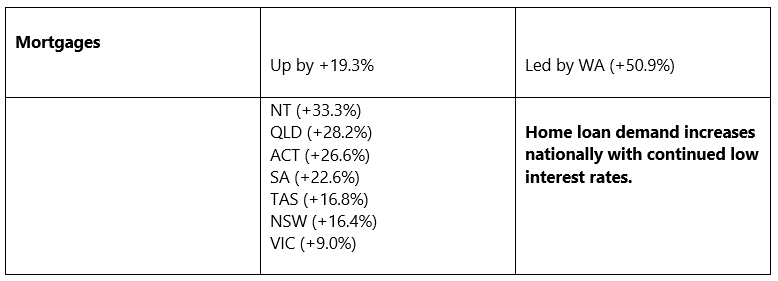

Mortgage applications increased by +19.3% (vs December quarter 2019).

Mortgage demand rises 19.3% in December Qtr

Equifax Quarterly Consumer Credit Demand Index: December Qtr 2020

Overall consumer credit applications down -21.9% (vs December quarter 2019)

- Credit card applications reduced by -31.7% (vs December quarter 2019)

- Personal loan applications dropped -28.1% (vs December quarter 2019)

- Buy now pay later applications trending down -1.5% (vs December quarter 2019)

- Auto loan applications decreased by -2.8% (vs December quarter 2019)

Mortgage applications increased by +19.3% (vs December quarter 2019).

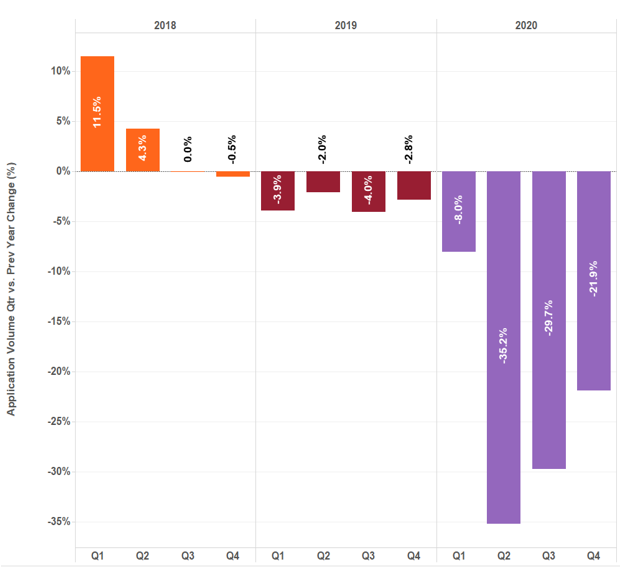

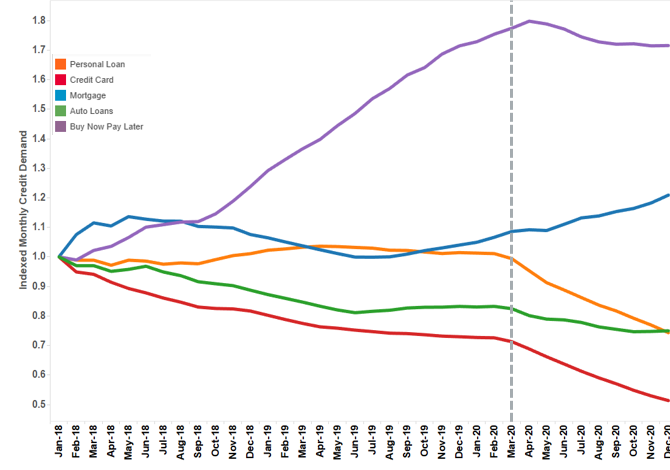

SYDNEY – 16 February 2021 – Consumer credit demand continued its decline in the December quarter, down -21.9% compared to last year but the rate of decline is slowing. According to data from the latest Equifax Quarterly Consumer Credit Demand Index (Dec 2020), while demand remained in decline, there are encouraging signs the rate of decline is slowing compared to the prior quarters of 2020. The fall in demand was largely driven by the continued decline in credit cards (-31.7%) and personal loans (-28.13%) with stronger signs of recovery in Buy Now Pay Later and Auto loans.

Released today by Equifax, the global data, analytics and technology company and the leading provider of credit information and analysis in Australia and New Zealand, the index measures the volume of credit applications for credit cards, personal loans, Buy Now Pay Later (BNPL) and auto loans.

Despite a backdrop of a decline in unsecured consumer credit applications, mortgage demand continued to rise, with home loan applications for the December 2020 quarter up +19.3% from a year ago. The stand-out was Western Australia, recording the highest growth at 50.9%, likely as the result of improved consumer sentiment, Government stimulus for first home buyers and a more positive outlook for the mining industry.

Across the nation there was an increase in mortgage applications in the December 2020 quarter compared to the previous year. In addition to Western Australia, strong demand was seen in Queensland (+28.2%) and the ACT (26.6%). While growth in the largest real estate markets was not as strong, NSW increased +16.4% and Victoria showed positive signs with strengthened demand (+9%) versus the December quarter in 2019, as major lockdown restrictions eased.

Mortgage demand includes loans for new properties as well as re-financing. Historically, movements in Equifax mortgage application demand data have led changes in house prices by around six to nine months. Mortgage applications are not part of the Consumer Credit Demand Index but are a good indicator of home buyer demand and housing turnover.

Kevin James, General Manager Advisory and Solutions, Equifax said: “Despite the decline in overall credit demand year on year, we have seen some steady growth from the September quarter which is a positive sign following the more extensive COVID-19 lockdowns. This has been driven by improvement in auto lending in many states, as well as personal loan applications. Across all states, the market showed strong resilience, even in Victoria which was affected by the second wave of COVID-19, with numbers in the last quarter of 2020 improving considerably.”

“Demand for mortgages has now experienced growth for the sixth consecutive quarter driven by low interest rates, stimulus for first home buyers and the HomeBuilder program, as well as Aussies returning home,” James said.

Demand for Buy Now Pay Later applications was relatively flat (-1.5%) in the December quarter compared to the previous year following two consecutive quarters of decline. ACT, NSW and NT all experienced growth which offset reductions in other states. Generation Z continues to be the strong driver of BNPL demand, making up 25% of total applications.

TABLE 1: Consumer Credit Demand by State

Mortgage Demand

IMAGE 1: Equifax Consumer Credit Demand Index –December 2020 Quarter

GRAPH 1: Consumer Macro Credit Demand – Quarterly YOY

GRAPH 2: Consumer Credit Applications – Indexed by Type

* The data has been re-indexed* from 2018 to account for the recent inclusion of Buy Now Pay Later applications:

Re-indexed data to commence in 2018 (previously 2015)

Added buy now pay later and auto loan credit enquiries as a separate trendline (previously rolled up into personal loans)

###

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employees, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by more than 11,000 employees worldwide, Equifax operates or has investments in 25 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

NOTE TO EDITORS

The Quarterly Consumer Credit Demand Index by Equifax measures the volume of credit card, personal loan, applications, Buy Now Pay Later and auto loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Q2 2026 analysis by Equifax Australia into consumer credit trends highlights how households are navigating ever changing economic conditions.