Credit active consumers looking to switch lenders

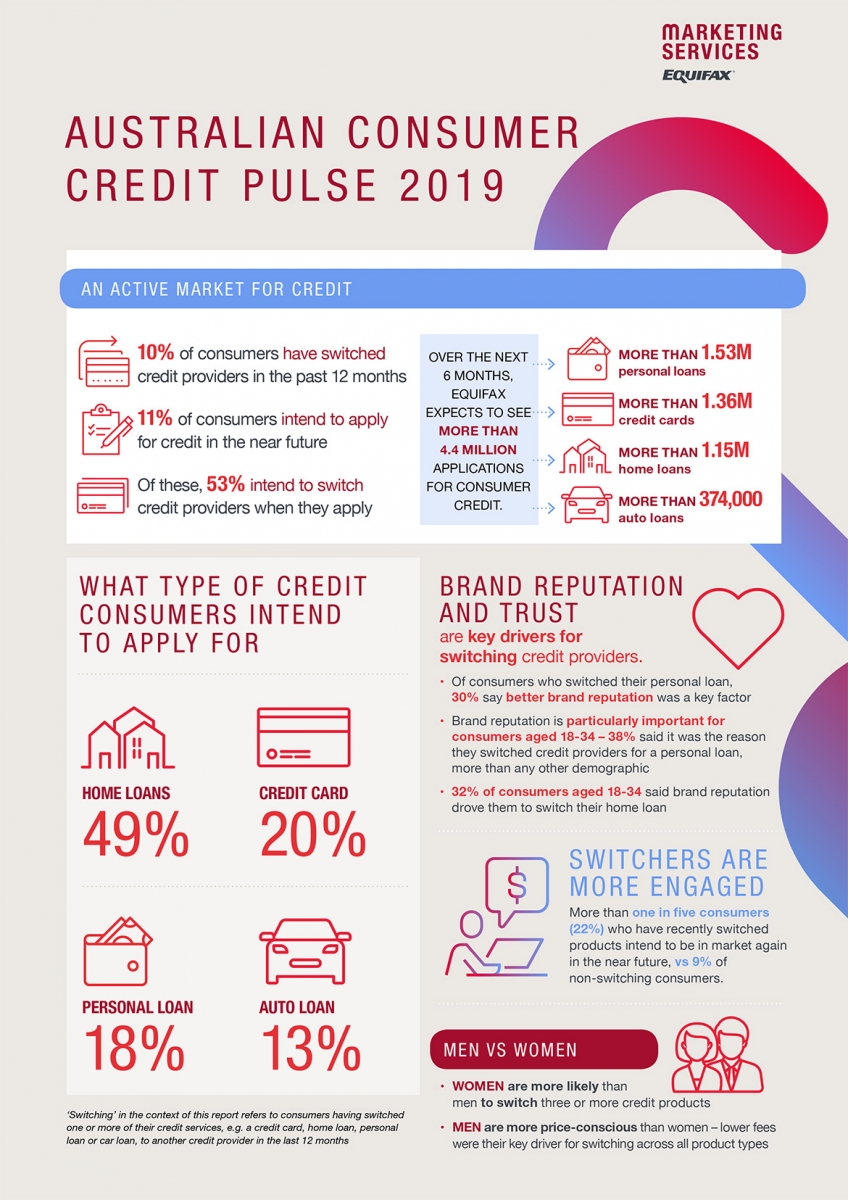

One in 10 consumers have switched credit products in the past 12 months, according to the Equifax Australian Consumer Credit Pulse 2019 report

SYDNEY, Wednesday, 31st July 2019 – One in 10 consumers have switched credit products in the past year, according to new research and analysis from Equifax, the global data, analytics and technology company and leading provider of credit information and analysis in Australia and New Zealand.

Released today, the Australian Consumer Credit Pulse 2019 report from Equifax also revealed that a further 11 per cent of consumers intend to apply for credit in the near future and, of these, 53 per cent are looking to switch providers when they make their application. The report draws on data analysis from the Equifax credit bureau developed to assist Australian entities with responsible lending obligations and other consumer protections, as well as for general public benefit.

James Forbes, General Manager, Marketing Services at Equifax, said the changing behaviours of once-loyal consumers presents both opportunities and challenges for banks and lenders.

“We expect to see more than 4.4 million applications for consumer credit in the next six months and, with consumer preferences rapidly changing, lenders need insight into what these applicants will be looking for,” Mr Forbes said.

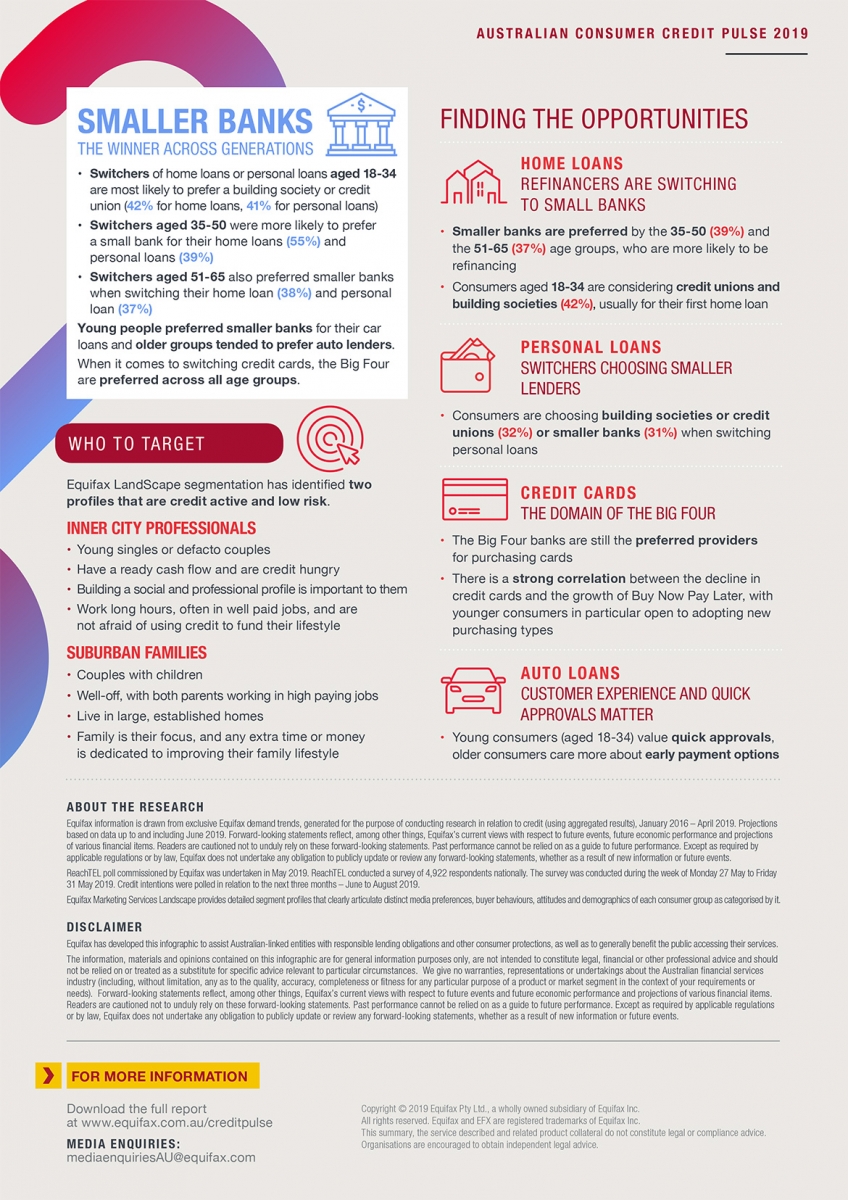

“Over the last 12 months the Big Four banks have ceased to be the first preference for many consumers who are switching credit products – instead, they’re increasingly choosing small banks, credit unions and building societies. For marketers, understanding what is causing this change in consumer behaviour is a great opportunity for lenders who want to attract and retain customers.

“Our research also shows the correlation between the decline of credit cards and the growth of buy now, pay later. While there are a number of factors at play here it does support the growing belief that consumers are opting out of traditional credit cards.” Mr Forbes added.

According to the report, the younger the individual, the more likely they are to be active in market for credit products, with 18-34-year olds being particularly mobile. Younger consumers are also more likely to switch lenders – of consumers who had switched in the past 12 months, 43 per cent were aged 18-34, and 32 per cent were aged 35-50.

Brand reputation was a key factor for this younger demographic when moving away from their provider, across all product types.

This demographic also has the greatest appetite for credit – younger consumers who have recently switched providers are more likely to apply for credit again in the near future than their older counterparts. Of this group, the largest volume is looking to apply for a home loan (41 per cent), followed by a credit card (25 per cent).

“There is a real opportunity for lenders to tap into the credit appetite of younger consumers and build long-term relationships based on brand reputation and customer experience – elements that this group is increasingly looking for in businesses and professional organisations,” Mr Forbes said.

Drivers of consumer switching behaviour

Unsurprisingly, lower costs were a major consideration for switching across all product types, with men being more price sensitive than women. However, consumers also cited better customer service and brand reputation as important considerations when switching products.

“In the wake of the Royal Commission, consumers are increasingly thinking about more than just cost when applying for credit. Now that reputation and customer service are coming into play, marketers need to be targeting customers with more than just a low-cost deal to retain them in the long run,” Mr Forbes said.

Finding the opportunities

Of the 10 per cent of consumers who have switched credit providers in the last 12 months, home loans and credit cards stood out as the big movers. A quarter (26 per cent) switched their home loans and nearly half moved their credit cards.

Home loans are also a popular product among the 11 per cent of consumers intending to apply for credit in the coming months, making up 49 per cent of intended applications.

For switchers of home loans or personal loans, those aged 18-34 were most likely to prefer a building society or credit union (42 per cent for home loans, 41 per cent for personal loans). Consumers aged 35-50 were more likely to prefer a small bank for their home loans (55 per cent) and personal loans (39 per cent).

“Understanding who is looking to apply for credit, and why, is half the battle for lenders. Armed with this type of information, marketers can offer products and services that speak directly to their target audience, helping them stand out in a crowded market,” Mr Forbes said.

Exploring consumer segments

The report also revealed that there are two key population segments, identified by Equifax Landscape profiles, that are both credit active and comparatively low risk – inner city professionals and suburban families.

Inner city professionals tend to be young singles or defacto couples who have a ready cash flow and are credit hungry. Building a social and professional profile is important to them; they work long hours, often in well paid jobs, and are not afraid of using credit to fund their lifestyle.

At the other end of the spectrum, suburban families largely comprise of couples with children. They tend to be well-off, with both parents working in high paying jobs, and many are in large, established homes. Family is their focus, and any extra time or money is dedicated to improving their family lifestyle.

“Offering one-size-fits-all products is no longer a feasible approach for lenders. Which consumer segments are most active in market, what is important to them and their relative credit risk are all pieces of the puzzle for lenders wanting to take advantage of a changing market,” Mr Forbes said.

About the research

Equifax credit information is drawn from exclusive Equifax demand trends, generated by its credit bureau for the purpose of conducting research in relation to credit (using aggregated results), January 2016 – April 2019

Projections based on data up to and including June 2019. Forward-looking statements reflect, among other things, Equifax’s current views with respect to future events, future economic performance and projections of various financial items. Readers are cautioned not to unduly rely on these forward-looking statements. Past performance cannot be relied on as a guide to future performance. Except as required by applicable regulations or by law, Equifax does not undertake any obligation to publicly update or review any forward-looking statements, whether as a result of new information or future events.

Equifax Marketing Services Landscape provides detailed segment profiles that clearly articulate distinct media preferences, buyer behaviours, attitudes and demographics of each consumer group as categorised by it.

ReachTEL poll commissioned by Equifax was undertaken in May 2019. ReachTEL conducted a survey of 4,922 respondents nationally. The survey was conducted during the week of Monday 27 May to Friday 31 May 2019. Credit intentions were polled in relation to the next three months – June to August 2019.

About Equifax

Equifax is a global information solutions company that uses unique data, innovative analytics, technology and industry expertise to power organisations and individuals around the world by transforming knowledge into insights that help make more informed business and personal decisions.

Headquartered in Atlanta, Ga., Equifax operates or has investments in 24 countries in North America, Central and South America, Europe and the Asia Pacific region, with the acquisition of Veda, a data analytics company and the leading provider of credit information and analysis in Australia and New Zealand. Combined the companies bring close to 170 years of data and insights experience to the marketplace.

Equifax is a member of Standard & Poor's (S&P) 500® Index and its common stock is traded on the New York Stock Exchange (NYSE) under the symbol EFX. For more information visit www.equifax.com.au.

About Equifax Marketing Services

Equifax Marketing Services brings together data and advanced measurement tools to build insights that help drive marketing success. With the largest volume of financial behavioural data in the region, we help customers identify and maximise their insights to better target, acquire and measure marketing and business outcomes.

Related Posts

Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.

Equifax can now share data via Snowflake Marketplace, giving brands and businesses access to fast and secure data sets including Australian consumer credit trends, consumer and commercial data.