Equifax Quarterly Consumer Credit Insights: March 2024

-

Unsecured consumer credit applications declined (-3.5% vs March quarter 2023)

- Credit card applications grew (+13.2% vs March quarter 2023)

- Personal loan applications fell (-4.6% vs March quarter 2023)

- Buy now pay later applications declined (-24.7% vs March quarter 2023)

-

Secured consumer credit applications decreased (-2.8% vs March quarter 2023)

- Mortgage applications fell (-4.5% vs March quarter 2023)

- Auto loan applications increased (+4.7% vs March quarter 2023)

SYDNEY – April 2024 – Signs of financial stress amongst consumers are accelerating, with demand for credit cards climbing and arrears increasing across several credit types, according to the latest Equifax Quarterly Consumer Credit Insights - March 2024.

Released today by Equifax, the global data, analytics and technology company and leading provider of credit information and analysis in Australia and New Zealand, the Quarterly Insights measure the volume of credit applications for credit cards, personal loans, buy now pay later (BNPL), mortgages and auto loans.

Unsecured credit demand, comprising credit cards, personal loans and BNPL, decreased -3.5% in the March quarter, driven by declining demand for personal loans (-4.6%) and BNPL (-24.7%). Despite the overall decline in unsecured credit demand, credit cards bucked the trend, with demand growing by +13.2% versus the same period 2023.

Kevin James, General Manager Advisory and Solutions, Equifax, said: “We’ve seen a significant uplift in credit card demand, with many Australians reaching out for unsecured credit to alleviate cost of living pressures. We’re also seeing strong growth in credit card limits, up 29% year-on-year, which means consumers are applying for more money on their cards.

“While demand for personal loans has dropped, arrears in this portfolio are rising. In fact, personal loan arrears of more than 30 days past due have hit their highest point since 2020. And we expect this trend to continue - personal loan arrears tend to peak in Q2, as festive season spending becomes due. Taken together, these trends across credit cards and personal loans paint a picture of growing financial strain for consumers,” Mr James said.

Secured credit demand, derived from mortgages and auto loans, decreased -2.8% in Q1 2024 compared to the same period in 2023.

Mortgage demand fell -4.5% in the March quarter 2024 compared to the same period the previous year, reversing the positive growth seen in the previous quarter. Auto loan demand grew +4.7% in Q1 2024 vs the same quarter 2023.

“Over the past year, refinancing has been a key driver of mortgage demand as consumers who were reaching the end of their fixed rate period sought out better deals. Many of these mortgage holders have now refinanced and this demand has dropped off,” Mr James said.

Although mortgage demand has fallen, average limits and arrears continue to rise.

“While mortgage demand has declined, the average limit per new mortgage account continued to grow at a consistent pace of 7% year-on-year - reflecting increasing house prices.

“Additionally, we’ve seen higher mortgage stress this quarter despite stable interest rates; mortgage arrears increased across all categories. Arrears of 30-89 days past due increased 15% year-on-year, while arrears of 90+ days past due were up 17%,” Mr James said.

IMAGE 1: Consumer Macro Credit Demand – Quarterly YOY

Source: Equifax

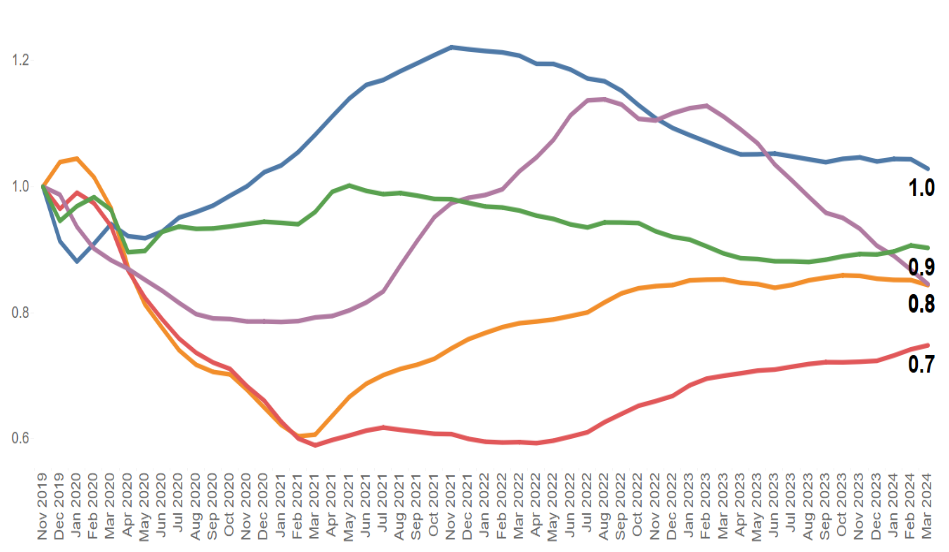

IMAGE 2: Consumer Credit Applications – By Type (Indexed to Nov 2019)

Source: Equifax

^The data has been re-indexed from 2018 to account for the recent inclusion of Buy Now Pay Later applications:

Re-indexed data to commence in 2018 (previously 2015)

Added buy now pay later and auto loan credit enquiries as a separate trendline (previously rolled up into personal loans)

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employers, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by nearly 15,000 employees worldwide, Equifax operates or has investments in 24 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

[email protected]

NOTE TO EDITORS

The Quarterly Consumer Credit Insights by Equifax measures the volume of credit card, personal loan applications, Buy Now Pay Later, mortgages and auto loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.

Equifax can now share data via Snowflake Marketplace, giving brands and businesses access to fast and secure data sets including Australian consumer credit trends, consumer and commercial data.