Equifax Quarterly Commercial Insights: March 2024

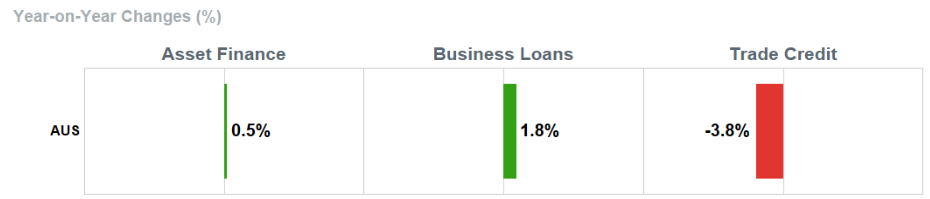

- Overall business credit applications increased by +0.7% (vs March quarter 2023)

- Business loan applications rose by +1.8% (vs March quarter 2023)

- Trade credit applications fell by -3.8% (vs March quarter 2023)

- Asset finance applications increased marginally, up +0.5% (vs March quarter 2023)

SYDNEY – May 2024 – Commercial credit demand grew moderately in Q1 2024 while insolvency levels rose to the highest point since 2015, according to the latest data from Equifax, the leading provider of credit information and analysis in Australia and New Zealand.

According to the Equifax Quarterly Commercial Insights - March 2024, commercial credit demand increased by +0.7% in Q1 2024 compared to the same quarter the previous year. This was driven by growth in business loan applications (+1.8% vs the same period in 2023) and a marginal increase in asset finance applications (+0.5%), although trade credit applications declined -3.8%.

Insolvency rates at the total market level increased by +41.1% in the March quarter 2024 vs the same period in 2023, and are up +145.7% on the same quarter in 2022. Additionally, Days Beyond Terms (DBT) - the average time taken to pay back dues - has increased year-on-year, bringing the average DBT to 6.5 days. The construction industry continues to outpace the market, paying their dues on average 10.2 days beyond terms.

Scott Mason, General Manager Commercial and Property Services, Equifax, said: “The total number of insolvencies in March surpassed the previous highest monthly insolvency volume, which was recorded in September 2015. The ongoing growth in insolvencies raises questions about the survivability of many businesses - particularly those, like the SMEs and sole traders in construction and hospitality, that are facing financial stress in both their professional and personal lives.”

According to Equifax data, sole traders and small business owners in the construction and hospitality sectors are significantly more likely to be in mortgage arrears than consumers with no commercial commitments, indicating growing financial strain.

“Across the board, many Australian consumers are struggling, with data from our consumer bureau showing that early stage mortgage arrears are up 30% in the last quarter compared to 2 years ago,” Mr Mason said.

“Given this overall increase in arrears, it’s of even greater concern that sole traders and SMEs in the construction and hospitality sectors are significantly more likely to be facing mortgage stress. According to Equifax data, sole traders in construction are 60% more likely to be in early mortgage arrears versus the average consumer, and SMEs in this sector are 30% more likely to be in arrears. Similarly, sole traders in the hospitality sector are 75% more likely to be in early mortgage arrears than the average consumer.

“Construction sole traders and SMEs in different regions across Australia have varying levels of stress. Sole traders based in Western and South Australia are twice as likely to be in early mortgage arrears versus consumers with no commercial commitments, while those in Victoria are 44% more likely.

“These business owners are having to make some extremely difficult choices around whether to prioritise paying their business or personal expenses and, as a result, their mortgage repayments are starting to lapse.”

Business credit demand March 2024 vs March 2023:

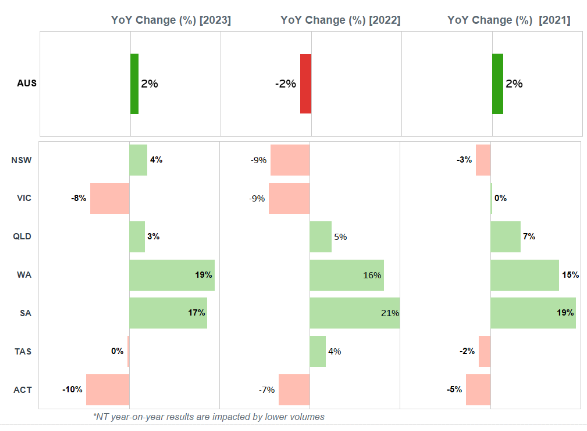

Overall business credit applications increased slightly (+0.7%) in the March quarter 2024. WA (+14%) and SA (+11%) experienced strong positive growth, followed by QLD (+2%) and NSW (+1%). Conversely, ACT saw the largest decrease in business credit applications (-9%), followed by VIC (-6%) and TAS (-1%).

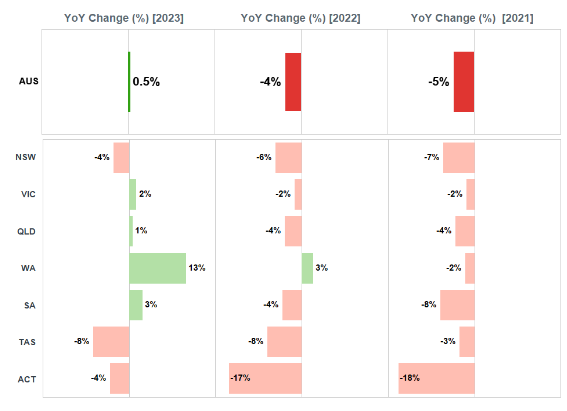

Business loan applications increased +1.8% in Q1 2024 compared to the previous year. ACT (-10%) and VIC (-8%) both experienced declines, while TAS (-0%) was flat. WA (+19%), SA (+17%) saw the greatest increases in demand, followed by NSW (+4%) and QLD (+3%).

Trade credit applications fell in Q1 2024 (-3.8%). TAS (+4%) and QLD (+1%) were the only states to experience an increase in demand. ACT (-10%) saw the greatest decrease in demand, followed by VIC (-6%), NSW (-6%), SA (-5%) and WA (-1%).

Asset finance (+0.5%) demand was flat in the March quarter. WA (+13%) experienced the biggest increase in demand, followed by SA (+3%), VIC (+2%) and QLD (+1%). TAS (-8%), NSW (-4%) and ACT (-4%) all experienced declines.

IMAGE 1: Equifax Commercial Credit Demand Index – March 2024 Quarter

IMAGE 2: Equifax Commercial Credit Demand Index by categories of credit – March 2024 Quarter

IMAGE 3: Business Loan Applications State Overview, 2024 Q1

IMAGE 4: Asset Finance Applications State Overview, 2024 Q1

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employers, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by nearly 15,000 employees worldwide, Equifax operates or has investments in 24 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

[email protected]

NOTE TO EDITORS

The Equifax Quarterly Commercial Insights (formerly Business Credit Demand Index) measures the volume of credit applications that go through the Equifax Commercial Bureau by financial services credit providers in Australia. Based on this, it is considered to be a good measure of intentions to acquire credit by businesses. This differs from other market measures published by the RBA/ABS, which measure new and cumulative dollar amounts that are actually approved by financial institutions.

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.

Equifax can now share data via Snowflake Marketplace, giving brands and businesses access to fast and secure data sets including Australian consumer credit trends, consumer and commercial data.