Equifax Consumer Market Pulse: Q4 2025

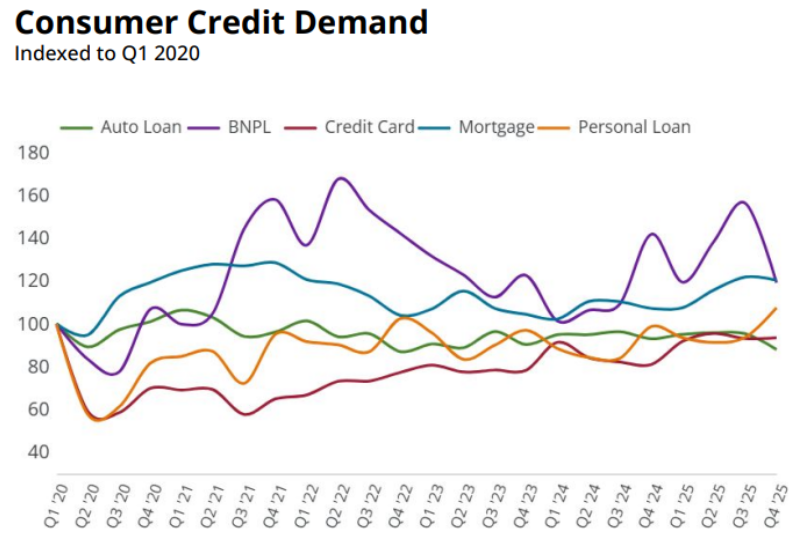

- Mortgage credit demand increased +12.3% (vs Q4 2024)

- Unsecured credit demand increased +5.9% (vs Q4 2024)

- Credit card demand increased +15.5% (vs Q4 2024)

- Personal loan demand increased by +8.9% (vs Q4 2024)

- Auto loan demand decreased by -5.4% (vs Q4 2024)

SYDNEY – 23 February 2026 – The latest Equifax Consumer Market Pulse for Q4 2025 reveals that Australians moved aggressively to secure their financial positions late last year, with mortgage enquiries increasing +12.3% year-on-year. This represents the most significant growth in mortgage demand observed since 2021.

Kevin James, Chief Solution Officer at Equifax Australia said, “This is a significant increase in mortgage demand, and a level of activity we haven't seen in nearly five years. It’s likely to have been supercharged by the government's expanded 5% First Home Buyer (FHB) Deposit Scheme that became available in October 2025, and buyers acting on the impression that rates had peaked in late 2025, and therefore rushed to lock in deals before the year's end.

“If this was their driver, they may have secured the last of the lower rates for a while, following the 25bps increase confirmed this February,” Mr. James added.

The Consumer Market Pulse for Q4 2025 shows that the mortgage demand surge was impacted by distinct demographic and regional trends.

Gen X (46–55 year olds) recorded the strongest mortgage demand growth at +13.6% YoY, while Upgraders - those increasing their mortgages for activities such as trading up to larger properties or major renovations - led loan purpose activity with a +16% YoY increase. First Home Buyer demand remained strong, rising by +11.2%, followed by a 9.6% lift in refinancing activity.

Geographically, the momentum was concentrated in the northern and western states. Queensland recorded the nation’s strongest mortgage demand growth with a +17% YoY increase, followed by Western Australia (+15%), and New South Wales (+13.5%). This geographical trend is also observed among FHBs.

“Within the First Home Buyer segment, mortgage demand this past quarter (Q4 2025) among Gen Z (18–30 year olds) was strongest Western Australia (+16.3% YoY) and Queensland (+14.1% YoY) - both states where prices exhibit relative affordability to those in New South Wales and Victoria.”

Aussie Mortgage Arrears Steady by Volume, but Loan Amount in Delinquencies up 6.8% YoY

The Consumer Market Pulse reveals that while the number of people failing to pay their mortgages remained unchanged, the dollar value of arrears debt rose by +6.8% YoY. Further to this the average loan amount at the late stage of delinquency has increased by +8.4% YoY, rising from $371k to $403k.

Arrears growth was most acute in Victoria (+16%) and New South Wales (+10.5% YoY), and Baby Boomers signaled signs of the most stress with the fastest rise in arrears among the age cohorts (+14.6% YoY) over the last quarter, closely followed by Millennials and GenZ ( 18–30 year-olds) at +11.3%.

According to Kevin James, “This increase in the dollar value of arrears debt for mortgages appears to correlate with higher house prices, potentially forcing buyers into larger loans that carry heavier repayment penalties.”

He added, “This pattern of older Australians (aged 66+) carrying this type of debt into retirement is something to keep an eye on, particularly if the rate environment continues to increase”.

Gen Z returns to plastic credit with a second quarter of double digit growth

The Consumer Market Pulse identifies that the unsecured credit demand appetite has been intensifying, contributing to a +5.9% YoY overall rise (compared to Q4 2024), as both credit cards (+15.5%) and personal loans (+8.9%) posted significant growth.

“Interestingly, in Q4, we saw double digit growth (+15.5% YoY) in the demand for credit cards. What struck me about this is that it was younger Gen Z’s aged 18-25 driving this - with a 23.2% surge in demand. In fact, it’s the highest rate of growth we’ve seen among this cohort for credit cards in three years, and likely due to the wave of aggressive credit card incentive campaigns in the market during the past quarter.’

“However, a significant concern has emerged among these younger borrowers, as they are also driving a +28.8% surge in credit card arrears.”

“In a decisive move to protect both the market and the consumer, lenders seemed to have tightened credit card limits, evidenced by a -8.3% year-on-year drop in average limits for new credit cards and a -3.9% decrease for personal loans. This proactive reduction appears to represent responsible lending in action, as banks prioritise stability over high-risk growth."

When looking at Personal Loans, despite an 8 basis point improvement in delinquency rates for personal loan arrears, the financial cost looks to have ultimately escalated, with the total limits associated with late arrears (90+days) having jumped by +10% YoY.

Examining this trend Kevin James said, “We're seeing a 'fewer but deeper' trend in personal loan debt. While the number of people falling behind on personal loans has actually dropped, the amount of money they owe has significantly increased. Essentially, it seems that fewer people are in trouble, but those who are, are carrying much deeper debt."

...

Equifax Consumer Credit Demand by Product Type

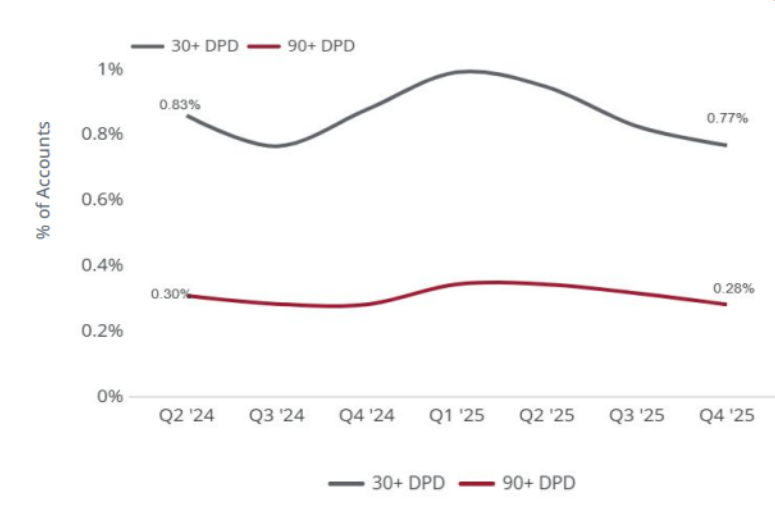

Credit Card Delinquency Rates – Accounts in Arrears as a Percentage of Portfolio

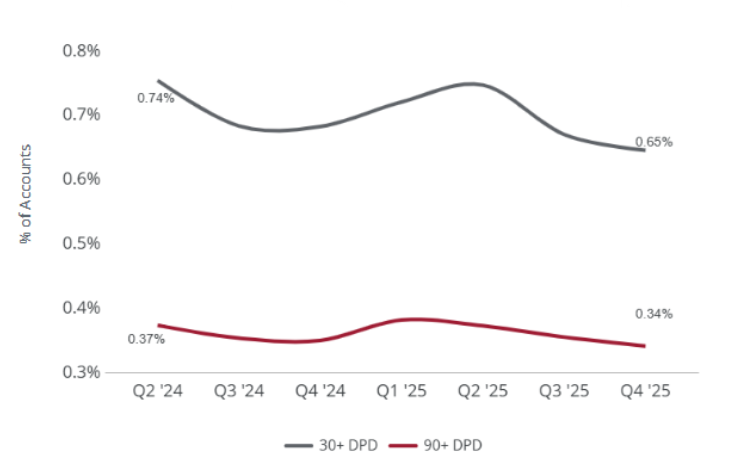

Mortgage Delinquency Rates – Accounts in Arrears as a Percentage of Portfolio

Source: Equifax

...

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employers, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by nearly 15,000 employees worldwide, Equifax operates or has investments in 24 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

[email protected]

NOTE TO EDITORS

The Equifax Consumer Market Pulse (formerly Consumer Credit Demand Index) measures the volume of credit card, personal loan applications, Buy Now Pay Later, mortgages and auto loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Key highlights:

KYC now requires a broader approach, blending identity data with behavioural data to identify risk patterns. Criminals are using complex corporate ownership structures to hide behind, making interconnected commercial data critical for KYB. Successful KYP needs to blend the technology of regular screening with interpersonal conversations to help detect risk.

Q2 2026 analysis by Equifax Australia into consumer credit trends highlights how households are navigating ever changing economic conditions.