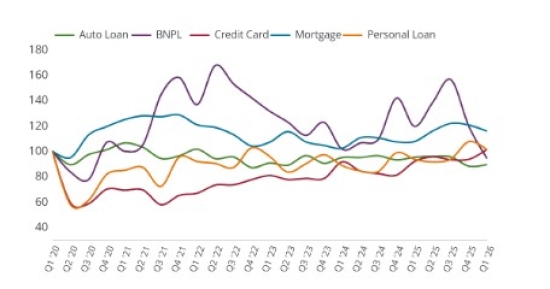

Economic conditions appear to be developing a similar trend to the 2022-23 post-Covid period - a time when the market faced a sharp 4.0% cash rate rise and inflation hitting 7.9%. Yet, during that period credit demand remained relatively benign rather than collapsing under the pressure. By drawing parallels between these two environments, Equifax observes that Australia’s consumer credit market may well be more durable than is often reported.

Lessons from the 2022-23 period

Following the pandemic, the economy entered a phase of significant volatility that tested the limits of household finances. While there was widespread alarm regarding a potential ‘mortgage cliff’, Equifax data revealed that the impact on arrears occurred with a notable lag and was far less catastrophic than many predicted. During that period, credit card demand remained steady, and personal loans showed almost no change in delinquency rates.

While today’s fuel prices and supply constraints may create similar macroeconomic pressures, the steady-state of Q1 2026 data suggests a comparable level of fortitude to this 2022-23 period.

How Australians are borrowing more carefully

The Equifax Consumer Market Pulse Q1 2026 shows secured credit demand grew by 4.9% year-on-year (YoY), led by a 7.5% increase in mortgage applications. The nature of this growth is telling: it is driven primarily by upgrades and a strong influx of First Home Buyers leveraging the expanded 5% deposit scheme.

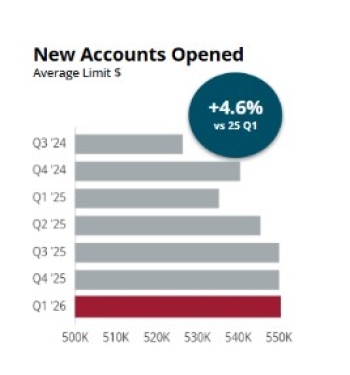

Consumers appear to be adopting a conservative posture, prioritising risk management and the search for better deals over aggressive new investment. While the total number of mortgage accounts decreased slightly by -0.3%, the average limit of newly opened mortgages rose by 4.6% to over $550,000, indicating that portfolio expansion is being driven by higher-value balances.

Arrears volume vs. value

A nuanced trend has emerged in late-stage arrears, where headline rates remain stable or are improving, even as the financial value of those arrears shifts. In the mortgage sector, 90+ days past due (DPD) accounts saw a 3 basis point reduction, with the total limits in late arrears falling by 2.2% compared to Q1 2025.

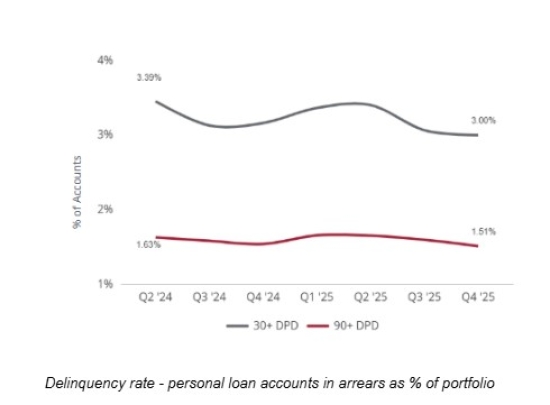

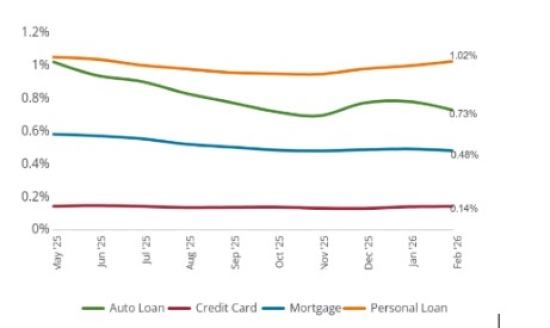

However, a divergence is visible in the unsecured space. Personal loan arrears volume improved by 14 basis points, yet the financial value of these late arrears rose by 3.1%, suggesting that stress is increasingly concentrated among larger balances. Similarly, credit card arrears showed improvement, particularly with a -10% reduction in delinquency among the 18-25 age demographic, contributing to a nearly 3% YoY decrease in the total financial value of card arrears.

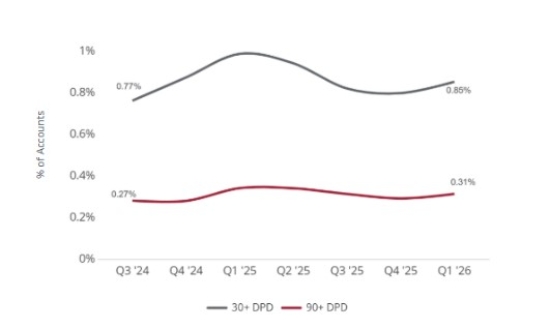

Delinquency rate - credit card accounts in arrears as % of portfolio

Unsecured lending churn and portfolio shifts

Unsecured credit demand remains robust, particularly in the credit card and personal loan sectors.

- Credit Cards: This sector marked its fourth consecutive quarter of double-digit growth, up 10.4% YoY. This is primarily driven by churn, as consumers actively seek better rewards or deals to offset cost-of-living pressures. Interestingly, new accounts opened actually fell by -3.7%, showing that high demand does not always translate to new portfolio growth.

- Personal Loans: Demand grew 7.9% YoY, a trend partly attributed to traditional Buy Now Pay Later (BNPL) providers expanding their offerings into the unsecured personal loan space.

Pockets of stress

Fig above: Hardship rate - accounts in hardship as % of portfolio

While the broader outlook remains resilient, this stability depends heavily on the labour market. Should unemployment begin to rise from its current low levels, the impact on consumer and commercial credit could become more pronounced.

Certain sectors, particularly those that are diesel intensive, such as transport, mining, agriculture and construction, are likely to be impacted by supply constraints in the near term. The construction industry continues to face pressure from fixed-price contracts and rising input costs for the likes of diesel and plastic piping, which can trap builders between escalating expenses and stagnant revenue, leading to insolvency.

In this changing environment, verification of financial health remains essential. Overall financial hardship accounts only increased marginally in Q1 2026, with non-mortgage hardship accounts rising by 2.9% and mortgage accounts by over 0.4% compared to the prior quarter. Geographically, Victoria has recorded the highest mortgage hardship rate at 0.70%, indicating localised areas of elevated stress.

The path ahead

The takeaway is one of cautious optimism. With the Middle East conflict and rising fuel prices continuing to shape the landscape, real-time data intelligence is more critical than ever. A trusted, global leader in data, technology and analytics, Equifax can help your business:

Monitor relationships with at risk sectors

- Proactively manage credit risk and hardship

- Identify resilient growth opportunities in a changing market

- Anticipate credit loss and bad debt provisioning with greater accuracy.

Contact Equifax

Source of data: Equifax Consumer Market Pulse Q1 2026