Business Credit Demand Bounces Back

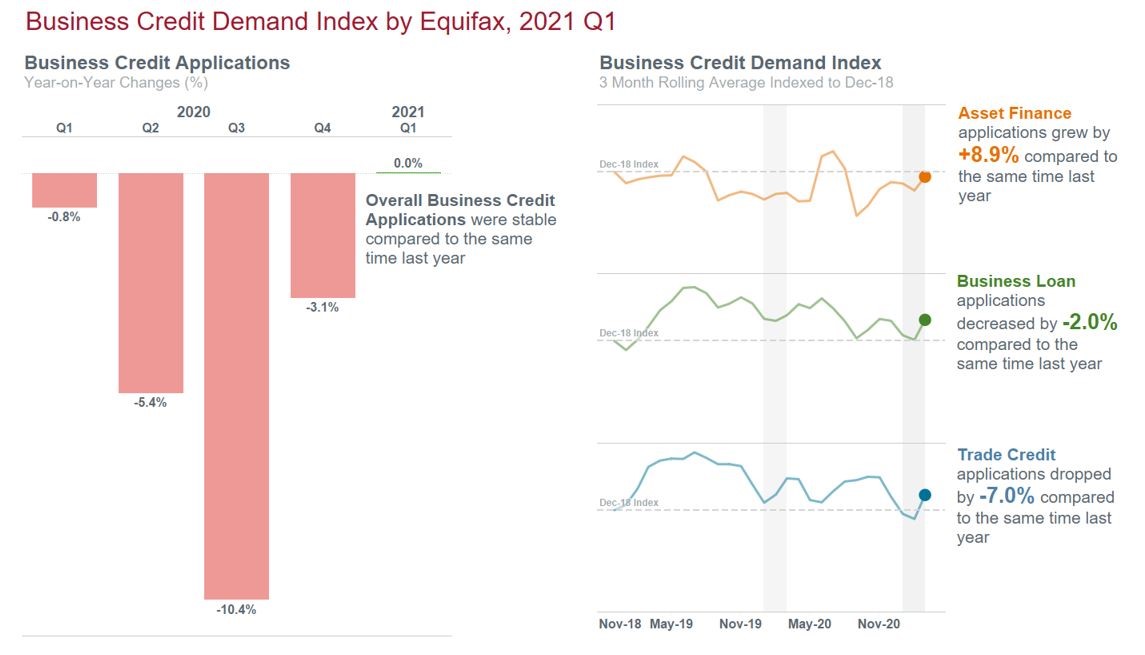

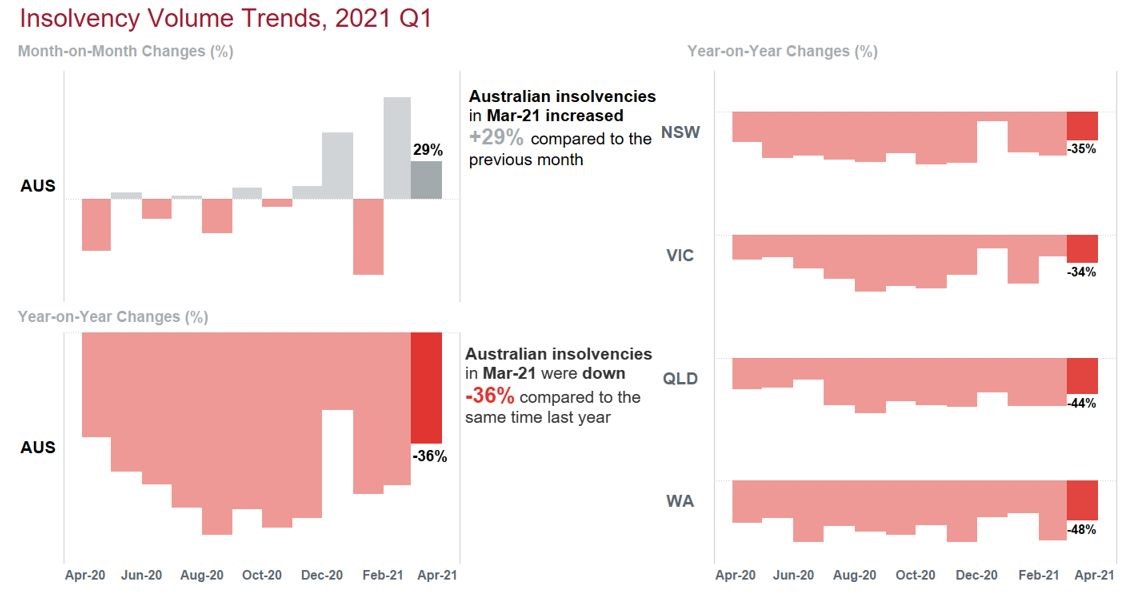

Business credit demand has returned to the same level it was in the March 2020 pre-pandemic quarter, driven by a bounce-back in asset finance (+8.9%). Business insolvencies have yet to match their March 2020 level (down -36% compared to March last year) but are rising, month on month up by +78% in February and +29.0% in March, according to the latest Equifax Quarterly Business Credit Demand Index (March 2021).

Business Credit Demand Bounces Back

Insolvencies rising but not yet at pre-COVID levels

Equifax Quarterly Business Credit Demand Index: March 2021

- Overall business credit halted their decline at 0.0% (vs March quarter 2020)

- Business loan applications decreased by -2.0% (vs March quarter 2020)

- Trade credit applications fell -7.0% (vs March quarter 2020)

- Asset finance applications increased by +8.9% (vs March quarter 2020).

SYDNEY – 5 May 2020 – Business credit demand has returned to the same level it was in the March 2020 pre-pandemic quarter, driven by a bounce-back in asset finance (+8.9%). Business insolvencies have yet to match their March 2020 level (down -36% compared to March last year) but are rising, month on month up by +78% in February and +29.0% in March, according to the latest Equifax Quarterly Business Credit Demand Index (March 2021).

Released today by Equifax, the global data, analytics and technology company and the leading provider of credit information and analysis in Australia and New Zealand, the index measures the volume of credit applications for trade credit, business loans and asset finance.

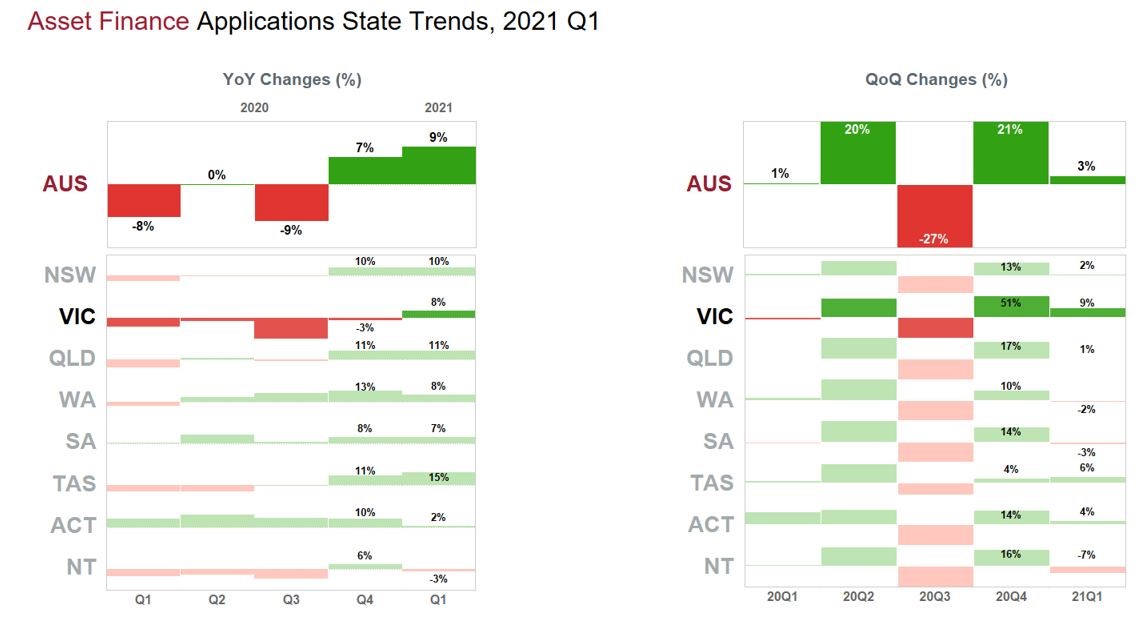

The March 2021 quarter has seen solid commercial demand, with overall business credit applications on par with the same period last year before the pandemic border closures and lockdown measures were implemented in late March 2020. Victoria also continues to rebound, down by only -3.0% this quarter compared with -12.0% the previous quarter.

This uptick in credit activity was fuelled by a large volume of credit information requests relating to asset finance (+8.9%), predominately from auto finance lenders (+25.0%). Demand for asset finance was also strong in the construction industry, where enquiries were up +10.0%.

Scott Mason, General Manager Commercial and Property Services, Equifax, said: “To see a rise in asset finance demand is a good sign for the economy demonstrating that businesses are starting to once again spend on replacement and renewal of equipment. The construction industry is a big user of asset finance, and this is the second quarter in a row applications have risen as the industry seeks to scale and grow.

“The expansion of the instant asset write-off scheme has also encouraged businesses to bring forward their spending on new assets, knowing they can claim a tax deduction upfront for the full value of the purchase.”

Business loan applications decreased by -2.0% in the March 2021 quarter but were unchanged compared with the December 2020 quarter. Head-to-head with the previous quarter, business loan applications in Victoria rose by +2.0% to draw even with Queensland and overtake NSW.

The worst performer was trade credit (-7.0%) compared to the prior year, but applications were slightly up in the March 2021 quarter compared to the prior quarter (+1.0%). In Victoria, trade credit applications also improved quarter to quarter.

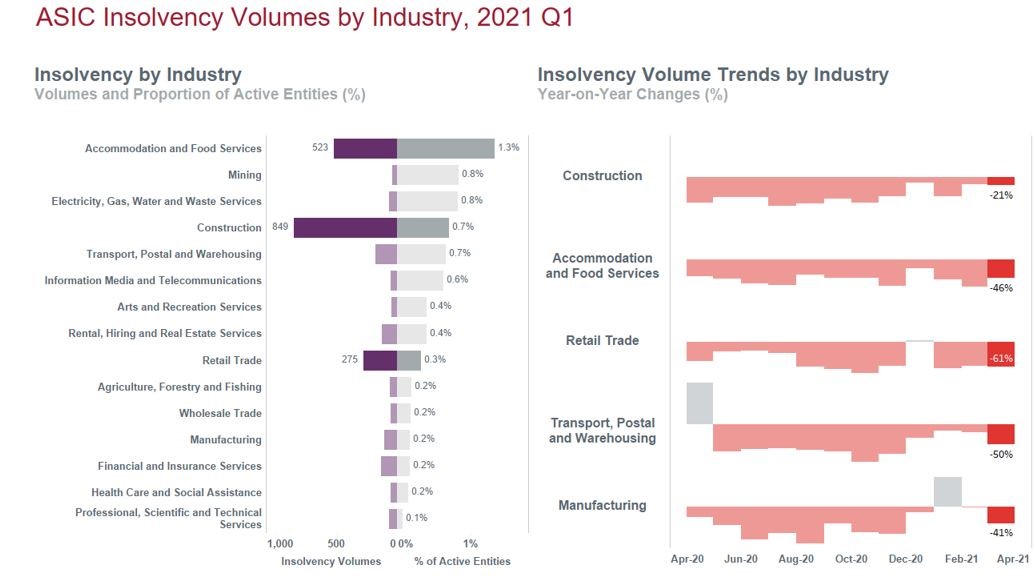

Insolvency volumes (-36.0% compared to March 2020) are yet to make a significant shift, but they are rising month on month by +78% in February and +29.0% in March.

“We expect it won’t be long before insolvency volumes return to their historical norms, particularly with JobKeeper now removed. Equifax analysis shows that corporate insolvencies are likely to dramatically increase over the next twelve months, with particular risk across deferral and hardship populations,” said Mason.

Business credit demand March 2021 vs. March 2020:

Business credit applications stabilised (0%). Applications were stable in NSW (0%) and WA (0%) and up in NT (+10.0%)*, QLD (+4.0%), TAS (+2.0%) and SA (+1.0%). Applications fell only in the ACT (-1.0%) and VIC (-3.0%).

Business loan applications remained down (-2.0%). Applications were depressed in TAS (-7.0%), VIC (-6.0%), SA (-3.0%) and NSW (-2.0%). WA (0%) and the ACT (0%) experienced no change, while applications went up in the NT* (+19.0%) and QLD (+4.0%).

Trade credit applications dropped (-7.0%). Both VIC (-10.0%) and WA (-10.0%) experienced a similar drop. Also down were NSW (-8.0%), the ACT (-7.0%), and QLD (-4.0%). Tasmania (+5.0%) and the NT (+3.0%) moved upward and SA (0%) remained stable.

Asset finance applications show positive growth (+9.0%). Applications were up in TAS (+15.0%), QLD (+11.0%), NSW (+10.0%), VIC (+8.0%), WA (+8.0%), SA (+7.0%) and the ACT (+2.0%). NT experienced a drop in applications (-3.0%).

*Note low volumes

IMAGE 1: Equifax Commercial Credit Demand Index – March 2021 Quarter

IMAGE 2: Asset Finance Applications State Trends, March 2021 quarter

IMAGE 3: Insolvency Volume Trends – March 2021 quarter, Year on Year changes

IMAGE 4: ASIC Insolvency Volumes by Industry, 2021 Q1

ABOUT EQUIFAX

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employees, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by more than 11,000 employees worldwide, Equifax operates or has investments in 25 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

NOTE TO EDITORS

The Quarterly Business Credit Demand Index by Equifax measures the volume of credit applications that go through the Commercial Bureau by financial services credit providers in Australia. Based on this, it is a good measure of intentions to acquire credit by businesses. This differs from other market measures published by the RBA/ABS, which measure new and cumulative dollar amounts that are actually approved by financial institutions.

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.

Equifax can now share data via Snowflake Marketplace, giving brands and businesses access to fast and secure data sets including Australian consumer credit trends, consumer and commercial data.