Double-Digit Growth in Consumer Credit Demand

Rebound now hit by Pandemic Second-Wave

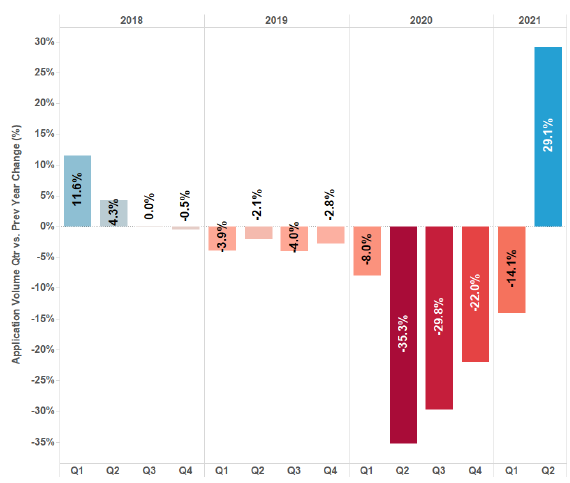

For the first time in three years, consumer credit demand has moved out of negative territory. According to the latest Quarterly Consumer Credit Demand Index (June 2021), demand recovered sharply in the June quarter (+29.1%), with applications for credit cards, Buy Now Pay Later (BNPL), personal loans, auto loans and mortgages all experiencing double-digit growth. A drop in the momentum of recovery is expected in the third quarter, with stay-at-home pandemic orders impacting around 10 million Australians

Equifax Quarterly Consumer Credit Demand Index: June 2021

-

Overall consumer credit applications increased by +29.1% (vs June quarter 2020)

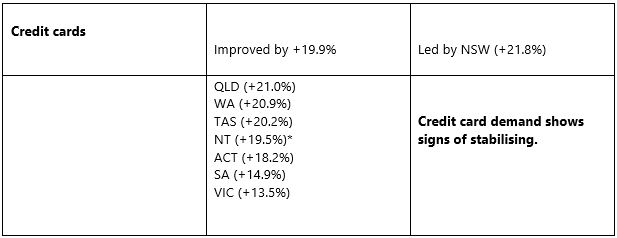

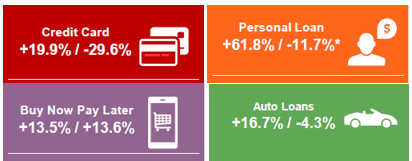

- Credit card applications rose by +19.9% (vs June quarter 2020)

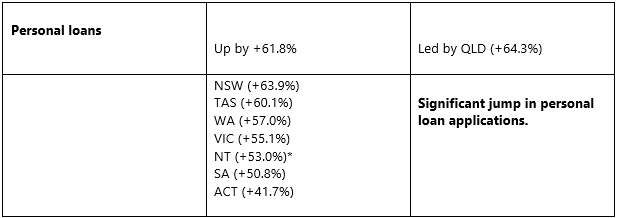

- Personal loan applications up +61.8% (vs June quarter 2020)

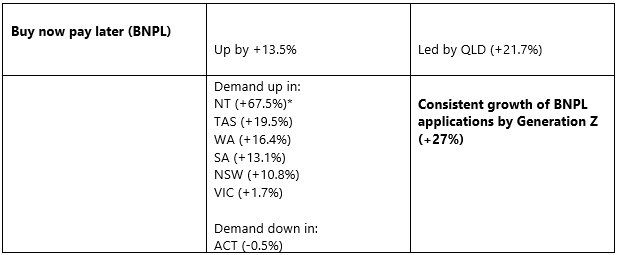

- Buy now pay later applications grew +13.5% (vs June quarter 2020)

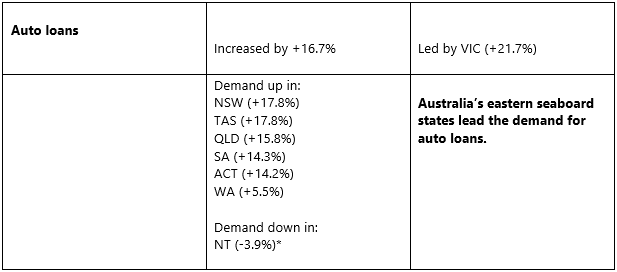

- Auto loan applications increased by +16.7% (vs June quarter 2020)

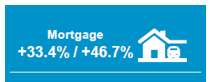

- Mortgage applications up +33.4% (vs June quarter 2020).

SYDNEY – 2 August 2021 – For the first time in three years, consumer credit demand has moved out of negative territory. According to the latest Quarterly Consumer Credit Demand Index (June 2021), demand recovered sharply in the June quarter (+29.1%), with applications for credit cards, Buy Now Pay Later (BNPL), personal loans, auto loans and mortgages all experiencing double-digit growth. A drop in the momentum of recovery is expected in the third quarter, with stay-at-home pandemic orders impacting around 10 million Australians – refer to image 1.

Released today by Equifax, the global data, analytics and technology company and the leading provider of credit information and analysis in Australia and New Zealand, the index measures the volume of credit applications for credit cards, personal loans, BNPL and auto loans.

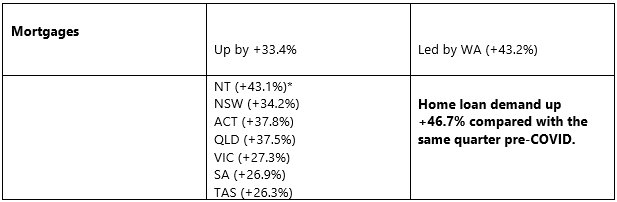

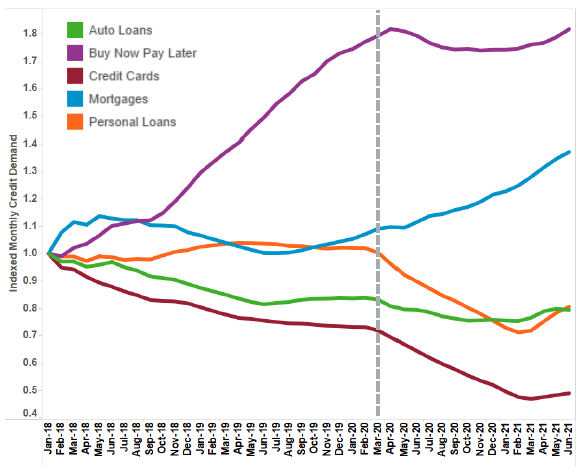

Strong consumer demand for housing continues to drive the growth of mortgage applications. Demand grew by +33.4% in the June 2021 quarter compared with the same period last year and +46.7% compared with the same period in 2019 pre-COVID. Western Australia recorded the highest mortgage demand (+43.2%), with the eastern seaboard states not far behind.

Kevin James, General Manager Advisory and Solutions, Equifax, said: “Mortgage demand has been consistent in its upward trajectory as low-interest rates and expanded government incentives continue to attract property buyers. The demand for home loans now far exceeds what it was in the same period pre-pandemic.”

Mortgage demand includes loans for new properties as well as re-financing. Historically, movements in Equifax mortgage application demand data have led changes in house prices by around six to nine months. Mortgage applications are not part of the Consumer Credit Demand Index but are a good indicator of home buyer demand and housing turnover.

Credit card demand defied its usual downward spiral in the June 2020 quarter by showing signs of market stabilisation (+19.9%). Personal loan demand also rose, and by a substantial leap (+61.8%), despite five consecutive quarters of decline.

“The growth in personal loan applications is strong and fairly uniform across Australia. What remains to be seen is what will be the impact of the latest state lockdowns on a return to pre-COVID levels,” James said.

BNPL applications grew steadily (+13.5%) in the June 2021 quarter. Queensland recorded the highest BNPL demand at 21.7%, and the ACT was the only area in Australia where demand went backwards (-0.5%).

While Generation Y holds the largest proportion of BNPL applications (+39.0%), demand is gradually shrinking across this cohort. Generation Z is moving ever closer to taking up the mantle, recording an increase in applications every quarter since 2018. In the June 2021 quarter, Generation Z accounted for +27.0% of demand.

The auto loan market was also in bounce-back (+16.7%) in the June 2021 quarter after a pandemic-induced slump this time last year. Recovery was particularly evident in Victoria (+21.7%) and the other eastern seaboard states but less so in Western Australia and the Northern Territory.

“With people opting out of public transport due to virus fears, demand for new and used vehicles has been escalating since last year. Although auto loan demand hasn’t yet returned to pre-COVID levels, it’s not far away,” James said.

TABLE 1: Consumer Credit Demand by State

Mortgage Demand

*Low volumes

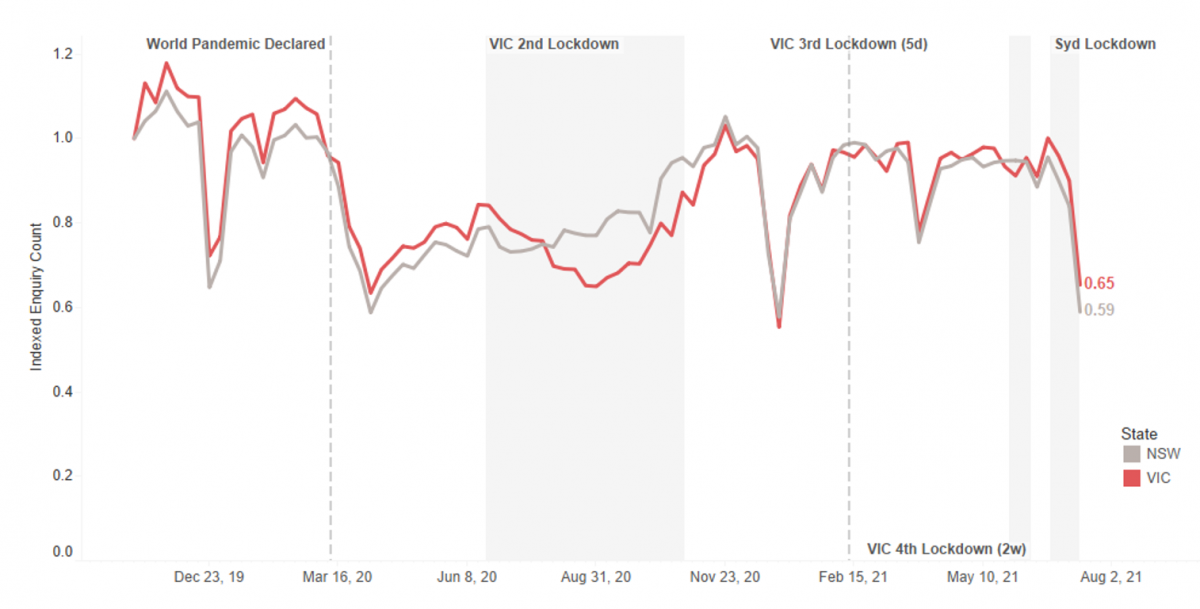

IMAGE 1: Consumer Credit Demand in NSW and Victoria – up until 15 July 2021

Note that enquiry trends are indexed against the first full week of Nov 2019 (4 Nov 2019 – 10 Nov 2019)

IMAGE 2: Equifax Consumer Credit Demand Index – June 2021 Quarter

Consumer Credit Demand

Quarterly Demand Change (vs Same Qtr 2020/2019)

* This figure has been adjusted to account for credit enquiries whose state information was absent in 2019.

Mortgage Demand

Quarterly Demand Change (vs Same Qtr 2020/2019)

IMAGE 3: Consumer Macro Credit Demand – Quarterly YOY

IMAGE 4: Consumer Credit Applications – Indexed by Type

* The data has been re-indexed* from 2018 to account for the recent inclusion of Buy Now Pay Later applications:

Re-indexed data to commence in 2018 (previously 2015)

Added buy now pay later and auto loan credit enquiries as a separate trendline (previously rolled up into personal loans)

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employees, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by more than 11,000 employees worldwide, Equifax operates or has investments in 25 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

NOTE TO EDITORS

The Quarterly Consumer Credit Demand Index by Equifax measures the volume of credit card, personal loan, applications, Buy Now Pay Later and auto loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.