Signs of Recovery Amid Continued Decline in Consumer Credit Demand

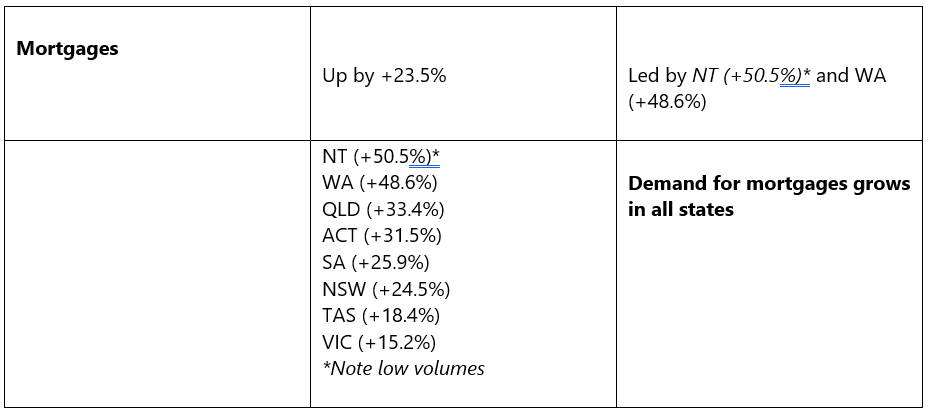

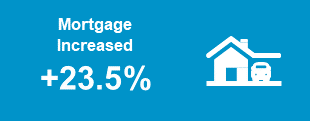

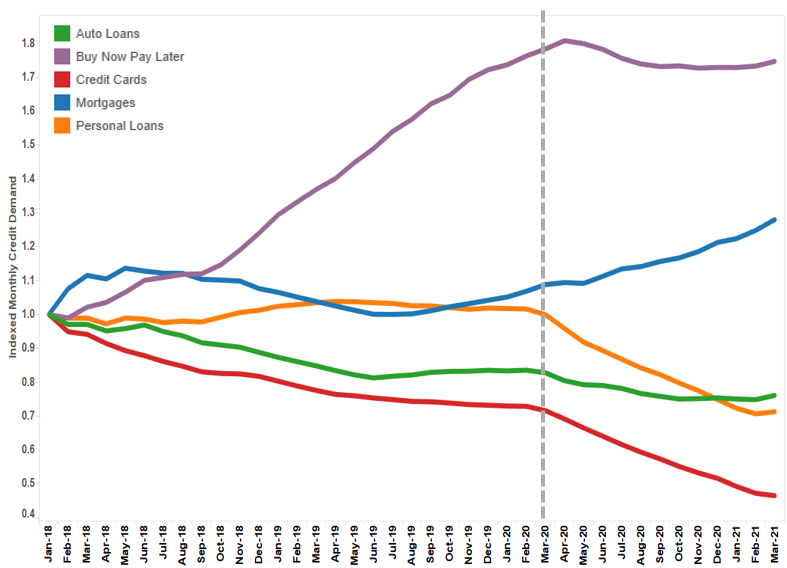

Consumer credit demand continues to decline compared to last year, but the rate of decline is slowing compared to previous quarters. Despite credit cards and personal loan demand remaining soft, auto loans and Buy Now Pay Later (BNPL) applications continue to recover, according to data from the latest Equifax Quarterly Consumer Credit Demand Index (March 2021). Demand for mortgages grew throughout Australia up +23.5% compared to the March quarter 2020, with every state and territory experiencing growth.

Equifax Quarterly Consumer Credit Demand Index: March 2021

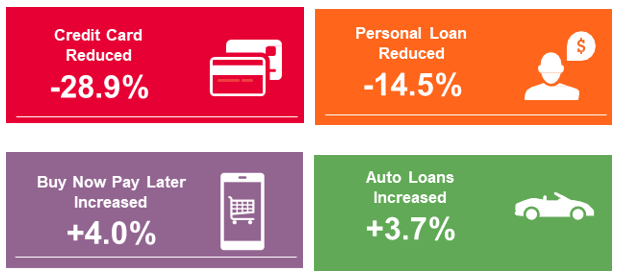

Overall consumer credit applications down -14.0% (vs March quarter 2020)

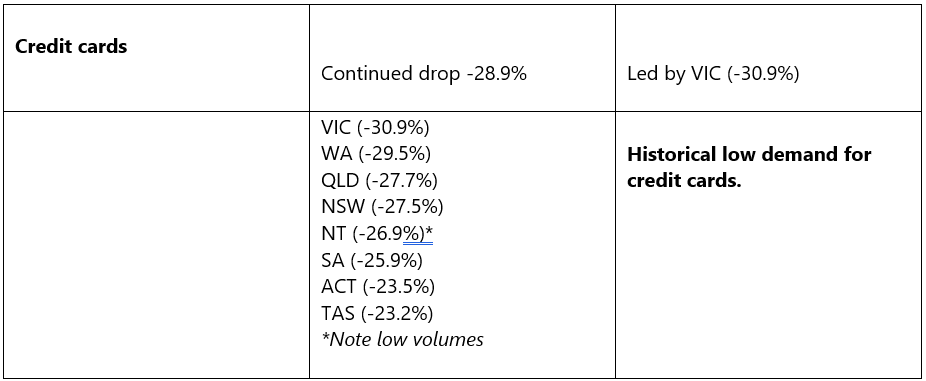

o Credit card applications declined -28.9% (vs March quarter 2020)

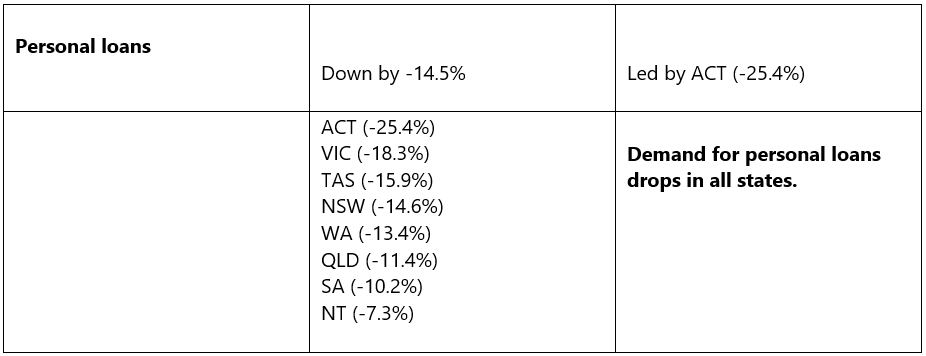

o Personal loan applications down -14.5% (vs March quarter 2020)

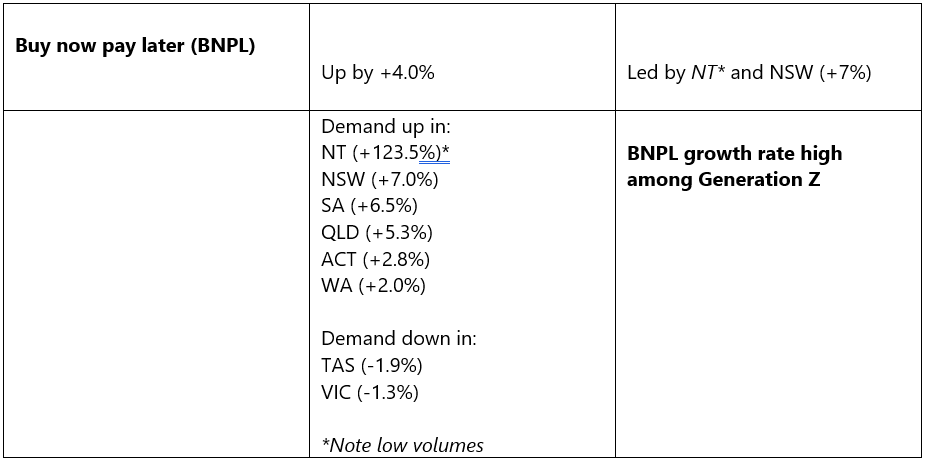

o Buy now pay later applications trending up +4.0% (vs March quarter 2020)

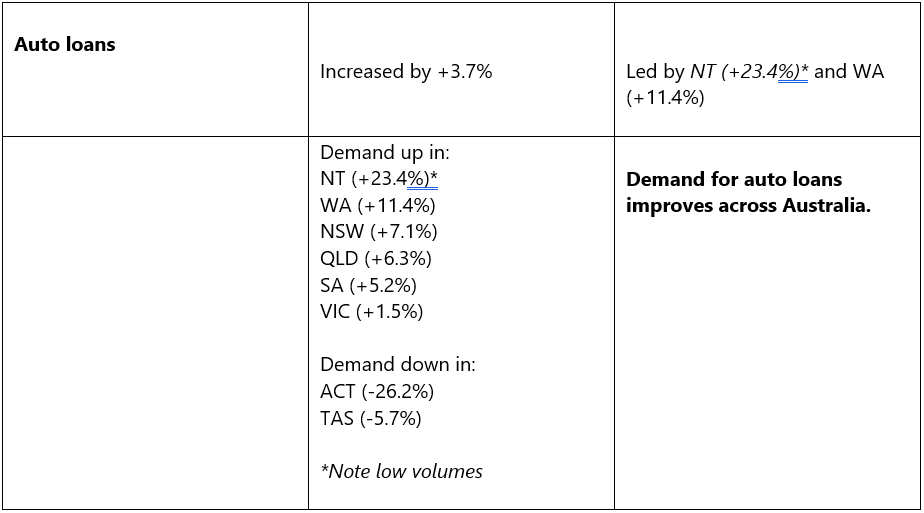

o Auto loan applications increased by +3.7% (vs March quarter 2020)

Mortgage applications up +23.5% (vs March quarter 2020).

SYDNEY – 29 April 2020 – Consumer credit demand continues to decline compared to last year, but the rate of decline is slowing compared to previous quarters. Despite credit cards and personal loan demand remaining soft, auto loans and Buy Now Pay Later (BNPL) applications continue to recover, according to data from the latest Equifax Quarterly Consumer Credit Demand Index (March 2021).

Nearly all states showed a rise in both auto loan applications (+3.7%) and BNPL applications (+4.0%) compared to the same period last year.

Released today by Equifax, the global data, analytics and technology company and the leading provider of credit information and analysis in Australia and New Zealand, the index measures the volume of credit applications for credit cards, personal loans, buy now pay later (BNPL) and auto loans.

Demand for mortgages grew throughout Australia up +23.5% compared to the March quarter 2020, with every state and territory experiencing growth. The eastern seaboard states continued to see an acceleration in home buyer activity, with Victoria showing a bounce back from a subdued previous quarter in lockdown.

Kevin James, General Manager Advisory and Solutions, Equifax, said: “The market is showing a shift to asset-based lending, with mortgages and auto loans proving more popular than liabilities like credit cards and personal loans.”

Mortgage demand includes loans for new properties as well as re-financing. Historically, movements in Equifax mortgage application demand data have led changes in house prices by around six to nine months. Mortgage applications are not part of the Consumer Credit Demand Index but are a good indicator of home buyer demand and housing turnover.

“Ultra-low interest rates are enticing more people into the market, but also an incentive for homeowners to refinance in the quest to find a better rate,” James said.

Credit card (-28.9%) and personal loan (-14.5%) demand remained down in the March 2021 quarter. Their decline has softened slightly compared to the previous quarter, but not enough to blunt their downward trajectory. This is the seventh consecutive quarter of decline for personal loans. For credit cards, the 12th straight quarter of decline. Victoria recorded the lowest demand for credit cards at -30.9%, while the ACT had fewer personal loan applications (-25.4%) than anywhere in Australia.

“Despite signs that the market may be moving towards post-COVID recovery, credit card demand continues to decline. The reduced economic activity in Victoria from their second lockdown didn’t help, but ultimately a change in consumer behaviour is pushing credit cards out of favour,” James said.

BNPL applications have improved following a brief slump in the previous quarter. Victoria and Tasmania were the only states not to show growth, but their volume of applications was still up on the last quarter.

“Demand for BNPL continues to come from Generation Y and Generation Z, but there are signs this cohort may have reached saturation. The younger generation – Generation Z – may soon catch up as they accounted for 26% of total applications. The lowest share remains with the baby boomer generation, not unsurprisingly since many are in retirement,” says James.

TABLE 1: Consumer Credit Demand by State

TABLE 2: Mortgage Demand by State

IMAGE 1: Equifax Consumer Credit Demand Index - March 2021 Quarter

Consumer Credit Demand

Mortgage Demand

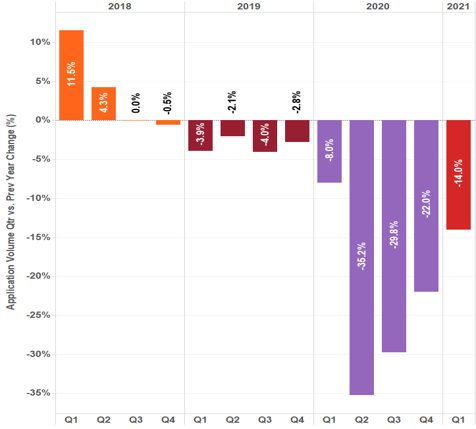

GRAPH 1: Consumer Macro Credit Demand – Quarterly YOY

GRAPH 2: Consumer Credit Applications – Indexed by Type

*Re-indexing:

Re-indexed data to commence in 2018 (previously 2015)

Added buy now pay later and auto loan credit enquiries as a separate trendline (previously rolled up into personal loans)

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employees, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by more than 11,000 employees worldwide, Equifax operates or has investments in 25 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

NOTE TO EDITORS

The Quarterly Consumer Credit Demand Index by Equifax measures the volume of credit card, personal loan, applications, Buy Now Pay Later and auto loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.

Equifax can now share data via Snowflake Marketplace, giving brands and businesses access to fast and secure data sets including Australian consumer credit trends, consumer and commercial data.