Equifax Market Insight: Navigating the current retail credit market

As lenders attempt to navigate through this period of enormous market uncertainty, Equifax will provide a series of regular analysis. While a clear picture of the future for credit markets is challenging in the short term, we hope to provide some clarity on what trends are developing, what challenges are foreseeable, how you can assess the risks to your portfolios and make prudent changes to your risk management controls.

External Environment

Over the last two weeks, there have been two significant announcements from the Federal and State governments. Firstly, social distancing controls have been significantly tightened and secondly additional economic stimuli have been agreed. Both are significant in their impacts on potential economic recovery.

How the COVID-19 situation plays out is uncertain and there are differing views on how this could occur. The Grattan Institute has published a comparison of two potential options in the Australian context1 that have different implications for credit markets and the economy:

- Eradication through a short (8-12 week) and severe shutdown period.

- Flattening the curve which requires controls to be in place for an extended period (12 months or more).

The Federal government has announced extraordinary economic stimuli to limit the impacts to the economy and protect jobs. The most significant of these is the JobKeeper allowance, designed to subsidise salaries for businesses that have seen a significant reduction in revenue. Bill Evans, Chief Economist at Westpac, has conducted an industry level analysis of the economic impacts and benefits from the JobKeeper policy, with the following high-level conclusions2:

- June quarter GDP to contract by 8.5%, with unemployment peaking at 9%

- September quarter GDP to contract by 0.6%

- December quarter GDP to lift by 5.2%, with unemployment recovering to 7%.

These measures being taken by the Federal government are important for credit risk management as they help to firm up scenarios of how a downturn may impact credit portfolios. These scenarios allow us to develop strategies to manage aggregate portfolio risk and formulate appropriate customer assistance.

Origination

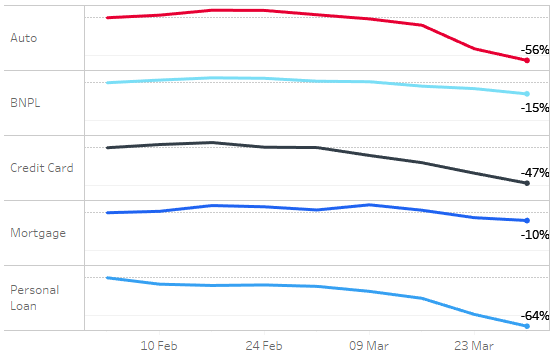

Weekly credit demand volumes are showing some significant short-term trends. Weekly Equifax credit enquiry volume trends to 29 March are shown in Figure 1. Observations as follows:

- Mortgage showing a modest fall at the end of March only, however, falls in the number of auctions and clearance rates3 may accelerate this trend

- Auto showing a drop in the second half of March

- Cards and Personal Loan (fixed) showing the most significant falls

- Buy Now Pay Later showing small declines in the second half of March.

Figure 1 – Weekly credit enquiry volumes, indexed to w/c 3 February 2020

Credit Risk Implications

The primary consideration for change to origination credit policy at this point remains stability of income. Immediate effects on unemployment and underemployment will vary significantly by industry, job type and individual employer. On the positive side, other industries may see an increase in employment and employed hours.

A responsible lending assessment requires inquiry and verification on income and inquiry about foreseeable changes in financial situation. It is likely that a significant proportion of applicants will have evidenced some change in the amount of income received, especially those employed on a casual basis or who receive regular overtime. As such, additional inquiry and verification may be required for many applicants for at least the remainder of 2020.

Lenders that utilise application or bureau scorecards as part of their origination process may have questions about the performance of these analytical tools in the current environment. We have observed both in Australia and overseas that scorecards generally continue to risk rank effectively, however the magnitude of default in each score band usually changes. We are currently finalising insights on scores performance for release shortly.

Portfolio Management

Many lenders are currently attempting to assess how different economic scenarios could impact their portfolios, and what measures they could deploy to mitigate negative impacts. At this time, the timelines for changes in economic controls are uncertain. The duration of controls will have an impact on employment and recovery in different industries. Government modelling scheduled for release4 in the coming weeks may help clarify this.

During this period of uncertainty, an appropriate approach is to consider a number of potential scenarios. These scenarios will all depend on the extent of shutdown periods whether it is a short eradication period or a longer term, flattening of the curve. It is also likely that these scenarios will need to be updated regularly as the government makes further announcements.

Government stimulus packages, in particular the JobKeeper payments, are designed to reduce the impact on unemployment. The Westpac modelling5 concluded that this stimulus could reduce peak unemployment from 17% to 9% in the June quarter. This is likely to have a significant impact on scenario assumptions.

Credit Risk Implications

The impact of government policy on social distancing, together with economic assumptions, particularly about unemployment rates are instructive for assessing risk mitigation strategies. Another key factor in assessing portfolio risk is the impact that the controls and economic downturn will have at an industry level, or for organisations that fail or who stand down employees. There have already been a number of retailers (Michael Hill, Myer, Premier Investments), airlines (Qantas, Virgin, Tiger) and travel agents (Flight Centre) who have made such announcements.

A number of credit providers have portfolios whose customer base has concentrations in certain industries. Quantifying portfolio concentration by industry as well as those with variable incomes (casual or overtime) could be instructive in determining what actions may be appropriate to manage.

Collections

As this crisis unfolds credit providers are experiencing significant requests for hardship assistance, with some portfolios now reaching more than 5% of accounts6 and growing. In these times, pragmatic leadership and data driven decisions will likely be the difference for both credit providers and customers in the short and long term. Many credit providers have been proactive with immediate 6-month payment deferrals and even interest refunds during that period. It would be remiss to think customers aren’t thinking that’s great but what happens in six months?

The potential issue with a blanket offering to all customers with a payment deferral is this will create a population that will need guidance and possibly more long-term solutions after six-months. There is no concrete answer to how long the economy and normal business operations will be impacted. Therefore, what should the hardship offering be? There is no one size fits all and understanding a customer’s situation is critical through open and direct conversations and validation. This can help uncover whether the customer has an underlying issue prior to the crisis that is now exacerbated further. Once this is known you can better match the solution to the customer’s situation.

There is a balance between volume management, customer expectations and risk management (short and long-term) that collections managers need to be mindful of. It is often said that a lender who is there for their customers in the hard times creates deep customer loyalty. This could be seen as an opportunity to tailor customer solutions and create real rapport, loyalty and above all else future customer retention when the economy mends.

Credit Risk Implications

The Global Financial Crisis (GFC) taught us that consumer behaviour changes in periods of economic volatility. As economic stimulus is implemented and measures are taken to protect consumers, there can be a natural change to what a consumer prioritises as important. Prior to 2008 consumers paid what they viewed as the most important commitment, their mortgage. During the GFC lenders were frowned upon to foreclose and take possession of properties. This resulted in credit cards rising to the top of the hierarchy of payments by consumers and mortgages prioritised last.

If we take the learnings from the GFC, decisions not to default or collect at all during this time could change consumer behaviour and potentially exacerbate an existing issue. Proactively analysing portfolios to identify vulnerable segments and non-impacted collectable segments is likely to be essential ongoing. Typical segmentation may begin to be less effective in the coming months and as a result a focus on data and analytics to refine segmentation and innovative digital strategies could be.

Finally, communication channels with customers will be key, not only in requests for assistance, but through the next six months or longer that arrangements are in place. Many credit providers and consumer groups are reporting delays in being able to make contact due to the volume of inbound requests.

Summary

Events continue to progress very quickly, but as we get a better view of the controls and economic stimuli that will be in place this should allow credit providers to better quantify scenarios for future performance, consider what provisions to make to maintain business continuity and develop customer assistance strategies. We hope through this series of analyses, that Equifax can assist in navigating these challenging times.

We are sure many of you are working from home as we are at Equifax. It is encouraging to observe broad acceptance of home environments with noise, kids, partners and pets in the background of videoconferences. We trust all of you and your teams have been able to transition to remote working without significant disruption.

Retail Credit Insights prepared by Stuart Musgrave, Principal Advisory Services Consultant, and Nick Jenkins, Debt Services Solution Consultant, Equifax.

2https://westpaciq.westpac.com.au/Article/42822

4https://www.health.gov.au/news/modelling-how-covid-19-could-affect-australia

Related Posts

Highlights:

Mitigate the surge in AI-generated digital forgeries by moving from document-based checks to source-verified payroll data Combat sophisticated salary staging and liar loans with an automated, single source of truth Establish digital trust at the point of contact to protect your organisation from credit and compliance risks.