Equifax One Score: Why It May Help Lenders Approve More Loans

For some credit applications, it’s a fast and straightforward decision whether to grant or deny approval. For others, evaluating a borrower’s credit risk isn’t as easy, requiring more time and work chasing up referrals and double-checking background information. These marginal applications are a drag on efficiency, slowing down processes and impacting profitability. Too many credit opportunities are rejected because not enough is known about an applicant at this early stage of the credit lifecycle.

The new generation Equifax credit score meets the need for a powerfully predictive analytic tool that informs a higher level of consumer credit risk prediction. Compared to previous Equifax scores, Equifax One Score gives lenders a substantial step up in accuracy for determining and quantifying risk.

Marcus Bruhn, General Manager Data Science, Equifax said: “Our new score enhances a lender’s ability to quickly and easily identify prospects who may have experienced financial difficulties in the past but who are now creditworthy.”

He explains that with this more reliable information on which to base credit decisions, lenders can match products with risk levels and offer credit opportunities to a broader range of applicants.

“It provides greater certainty around who is applying and what the real risk is. Using the score upfront, even before the underwriting stage, means you can quickly determine the best offer for each individual,” he added.

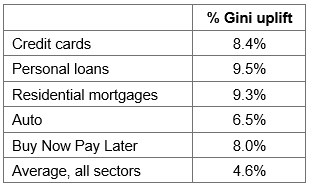

Looking at the gains in predictive lift

We put our previous generation score head-to-head with Equifax One Score. These model performance metrics1 show the Gini uplift2, demonstrating the gains in predictive power achieved with our new score.

For lenders, this Gini uplift in predictive performance translates to an upgraded ability to approve more consumers for credit without taking on additional risk. The strength of these gains is shown below.

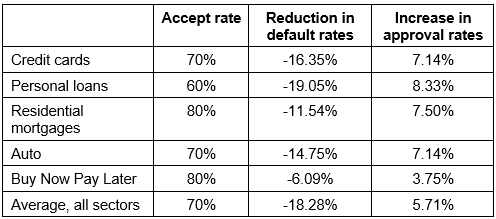

Using this modelling analysis3, lenders approving applicants in a low-risk portfolio like residential mortgages could reduce their default rates by 11.54% using Equifax One Score based on an acceptance rate of 80%. Equally, the number of applicants above the cut-off threshold could rise by 7.5% without changing the default rate. This equates to an 86% approval rate for the same risk.

There are performance gains in every portfolio, even the higher risk Buy Now Pay Later (BNPL) sector, where default rates were reduced by 6.09% based on an 80% accept rate. BNPL lenders could approve more loans without more risk – with a rise of 3.75% in their approval pool while maintaining the same default rate (83% approval rate for the same risk).

A step towards ending the disconnect

With the introduction of Equifax One Score, there will be a greater consistency in the credit score seen by a lender compared to a consumer. When lenders adopt the new score, the score that they will see when prescreening an applicant will now be the same as what the applicant sees when retrieving their credit score online4.

Bruhn explains that Equifax’s new generation score dynamically updates as credit-related information becomes available, both positive and negative. To ensure it remains resilient in changing times, Equifax One Score has been built to allow for more historical data and a greater breadth of information to close out some of the gaps left in the wake of the coronavirus.

“Previously, when a consumer applied for credit, their credit score was affected immediately by this enquiry. This change in the score was visible to the lender when assessing the applicant but not to the consumer when checking their online score.

“This discrepancy has been removed with Equifax One Score, so now current enquiry data won’t have the same point in time impact,” he said.

Now that there is a score common to both lenders and consumers, this champions a better customer experience and an improvement in financial literacy. Consumers have a greater incentive to manage credit responsibly once they can see through their score that there is a real relationship between positive credit behaviour and better financial deals. The flow-on effect is a greater demand for financial services and increased opportunities for lenders to boost their market share.

Equifax One Score gives lenders a step up in risk prediction. To find out more about how it delivers a more complete and consistent picture of a customer’s credit risk, recommended reading: Explainable AI for Credit Scoring.

1 This analysis does not consider lender policies or other underwriting criteria and uses the bureau scores as the sole criteria in loan approval for this comparison. The default rates are defined as any account that reaches 90 days past due or worse within 12 months after the date of the loan application being scored.

2 The Gini coefficient is a statistic which measures the ability of a scorecard to rank order risk. A Gini of 0% means that the scorecard cannot distinguish Good from Bad cases, and a Gini of 100% means that a scorecard distinguishes perfectly. Scorecards with Gini of 39% or over 40% are commonly used in credit assessment.

3 As above.

4 A time variance between the lender and the consumer viewing the score may result in a slightly different score outcome if something has changed on the consumers’ credit file.

Related Posts

Highlights:

Mitigate the surge in AI-generated digital forgeries by moving from document-based checks to source-verified payroll data Combat sophisticated salary staging and liar loans with an automated, single source of truth Establish digital trust at the point of contact to protect your organisation from credit and compliance risks.