What Auto Financiers Need to Know About Shadow Hardship

Auto financiers face a growing challenge that has been flying under the radar – shadow hardship. Equifax Senior Solutions Consultant Ashley Schumacher recently highlighted this issue at the 2023 Automotive Finance Forum. In this post, we’ll delve into what shadow hardship means, its implications for auto financiers and solutions to protect your business from this hidden pocket of risk.

Since July 2022, Financial Hardship Information (FHI) has been included in credit reports*. Comprehensive credit reporting (CCR) lenders, sharing repayment history information (RHI), now disclose if they have a temporary or permanent financial hardship arrangement with a customer. This broader insight paints a more comprehensive financial picture, offering better insight into default risk.

Yet, these risk signals may go undetected for lenders without this end-to-end visibility. Auto financiers who provide auto loans and rely on internal data for risk assessment could miss crucial insights into a customer’s overall financial performance. How would you know if hardship customers are lingering in your collection queue if you have no visibility into factors like mortgage delinquency or history of transactions outside the auto loan portfolio?

The shadow hardship concept

Schumacher introduced the concept of shadow hardship to refer to borrowers who actively manage hardship with some, but not all, of their lenders. These borrowers have multiple accounts across multiple lenders and may be trying to self-manage their way out of financial trouble at the risk of spiralling into deeper debt, or obtain finance without disclosing the full extent of any shadow hardship to prospective lenders.

An Equifax analysis of consumer repayment behaviour over time across a range of accounts from different financial institutions reveals vital insights about shadow hardship:

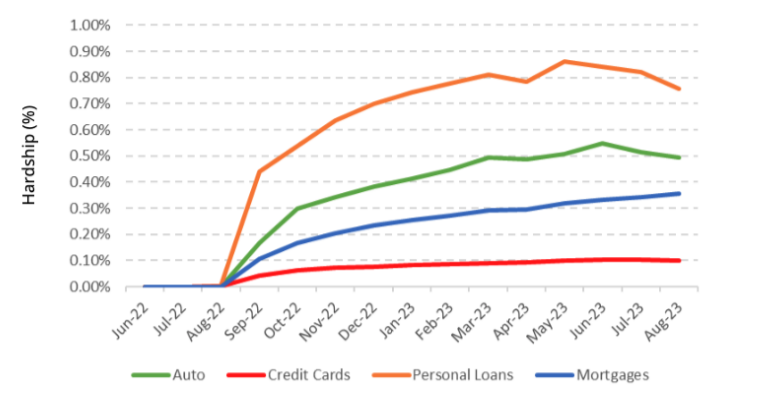

1. Mortgage hardship rates are on the rise

Mortgage hardship continues to climb, while non-mortgage hardship levels have stabilised. Our analysis shows that mortgage hardship has been steadily trending upward over an extended period, approaching 0.4% of reported accounts in August 2023.

While unsecured personal loan hardship has been tracking around 0.8%, there has been some levelling off in recent months. Auto loan hardship remains high, at approximately 0.5%, but it too is stabilising.

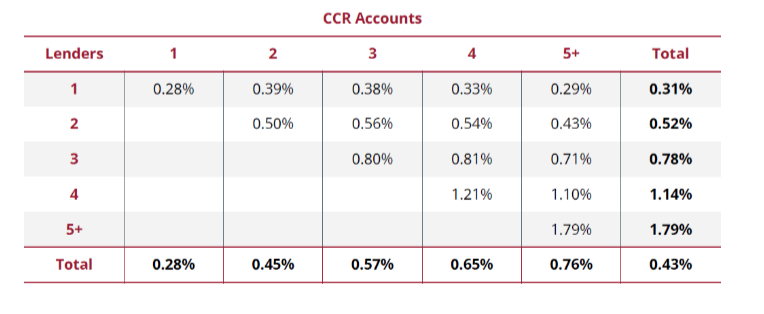

2. Customers with multiple lenders are more likely to be in hardship

The number of different lenders a borrower deals with matters more than the number of accounts they hold. Equifax analysis shows that borrowers with accounts across various lenders are at higher risk of hardship.

The top row of the above table shows the hardship rates for borrowers with one account/one lender through to borrowers with five accounts/one lender. These are the customers who have all their debt in one basket.

The hardship rate jumps substantially when borrowers hold multiple accounts across multiple lenders. For example, our analysis shows a hardship rate of 0.28% for a borrower with one account and one lender, compared with 1.79% for a borrower with five accounts across five lenders.

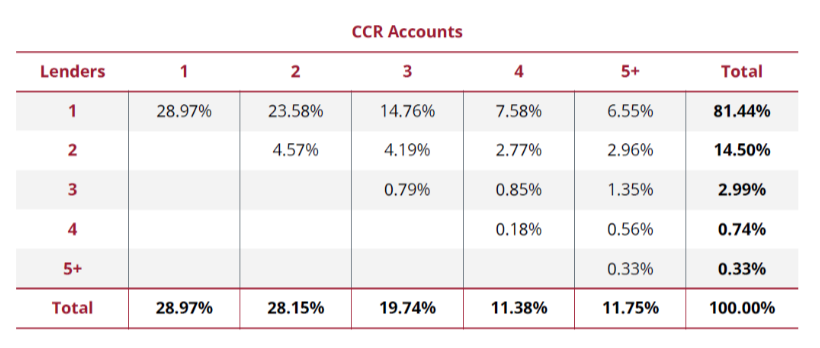

3. Most hardship customers also maintain non-hardship accounts

A significant portion of borrowers in hardship also maintain non-hardship accounts. From the above analysis, which shows the percentage of CCR accounts in hardship, we can see that customers with at least one account in hardship are unlikely to have their other accounts with other lenders in hardship.

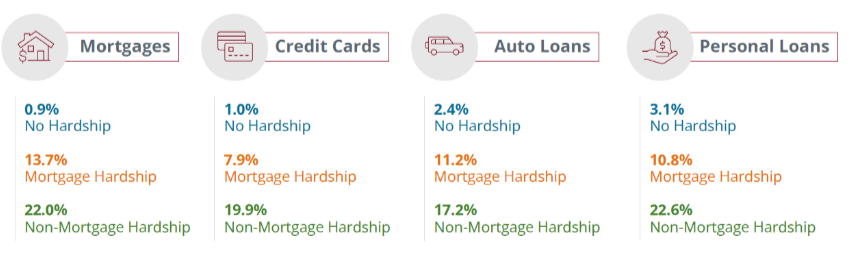

4. Customers in hardship accumulate arrears on their non-hardship accounts

Borrowers experiencing hardship tend to have high arrears on their non-hardship accounts, particularly auto and personal loans.

From our analysis of 30+ arrears on non-hardship accounts^, we can see the arrears rate of an auto loan customer not in hardship is 2.4%, yet this jumps to 11.2% if they are in mortgage hardship and 17.2% if they are in non-mortgage hardship.

Auto loans and personal loans are particularly vulnerable to shadow hardship because these loan types tend to rank lower in the financial priority of a borrower. When borrowers choose which accounts to rehabilitate first, our analysis shows they are more likely to prioritise their mortgage and credit card accounts.

Protecting your business from shadow risk

Enriching your internal data with Equifax data can help generate a broader, more holistic view of customers, their risk and your likelihood of recovery. Here are two examples of the ways in which data can be harnessed to uncover pockets of financial vulnerability within portfolios:

⦁ Onboarding: During the credit check process while onboarding, assess your borrower’s current indebtedness with other lenders and their history of hardship arrangements.. A deeper understanding of liabilities and account holdings across lenders can aid in risk prediction.

⦁ Back book: When customers enter collections, pull their credit report promptly to determine the most suitable treatment strategy for their situation. If they’re in hardship with other accounts, take preemptive measures to mitigate risk and offer proactive hardship assistance before they spiral into deeper debt. Identifying borrowers in need of extra support can help foster cooperation and improve customer retention.

As a leader in analytics solutions, we have the technology and expertise to reach wider and deeper into data sets, extracting insights that drive meaningful results. By transforming and connecting data, we make it possible to integrate insights into your workflow - fast, seamless, invisible - for decisions you can act on right away.

* FHI cannot be used in credit scores. The data is retained for 12 months and can only be disclosed where the consumer is seeking access to new credit. RHI during the arrangement must be reported.

^ Hardship levels recorded for Aug 2022 when credit providers started reporting their RHI and FHI data to Equifax.

Related Posts

Auto financiers face a growing challenge that has been flying under the radar – shadow hardship. Equifax Senior Solutions Consultant Ashley Schumacher recently highlighted this issue at the 2023 Automotive Finance Forum. In this post, we’ll delve into what shadow hardship means, its implications for auto financiers and solutions to protect your business from this hidden pocket of risk.

Veda and the Consumer Action Law Centre (Consumer Action) have agreed upon a conciliated resolution to the representative complaint lodged by Consumer Action with the Office of the Australian Information Commissioner (OAIC), in respect of Veda’s ABR Gazette commercial information service.