Equifax Australia hosted senior financial services leaders, risk executives, and compliance specialists at the Equifax Australia AML/CTF Summit 2026 to address the critical operational shift facing reporting entities following recent regulatory reforms.

Read more

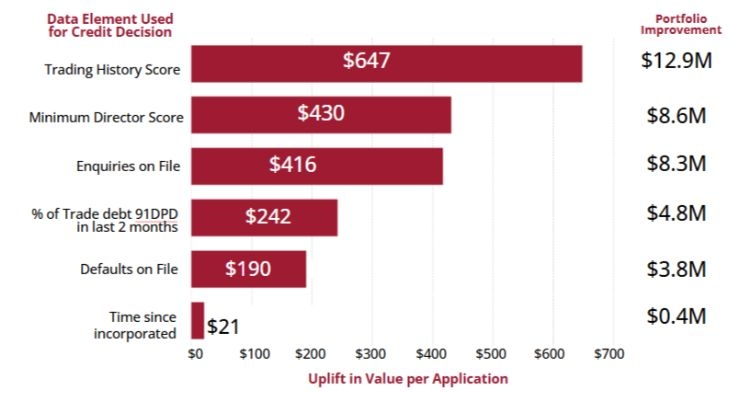

Data quality is a crucial element of effective risk management. Yet, credit decisions are routinely made with data that is inaccurate, duplicated, poorly compiled, incomplete or dated.

Understanding the criteria for a favourable iCIRT 'Conduct' assessment.

An iCIRT rating recognises the multifaceted elements that distinguish high-trust property development and construction companies. But what does this look like in practical terms?

Consumer confidence undercut by creeping debt as amount owed by some Australians increases

Economic uncertainty contributes to subdued business growth, while insolvencies hit a five-year high

The recent Equifax Frontiers: Championing Digital Trust event convened industry leaders to explore the evolving identity and fraud landscape. Discussions provided valuable insights into strengthening defences against fraud, scams, and data breaches, ensuring regulatory compliance, and future-proofing operations. The central theme emphasised that ‘digital trust’ - meaning customer confidence and security in online business interactions - is no longer a peripheral concern. Instead, it’s a foundational element for business resilience and growth. Consumers expect businesses to protect their personal data while offering transparent, reliable, privacy-respecting and frictionless digital interactions.

Here's a summary of the key insights and talking points from five of the top sessions.

New market leading CDR transaction-based risk score from Equifax harnesses the power of the Mastercard Open Banking platform to help consumers better understand their credit health and open new financial opportunities

The Equifax Q1 2025 Commercial Credit Report reveals a nuanced picture of the commercial credit landscape. Overall business credit applications saw a modest rise, but underlying trends reveal caution among Small and Medium Enterprises (SMEs) and significant pressures in key industries.

How effectively does your organisation detect potential money muling activities?