Post-election business credit demand boost short-lived

Veda Quarterly Business Credit Demand Index: September 2016 quarter

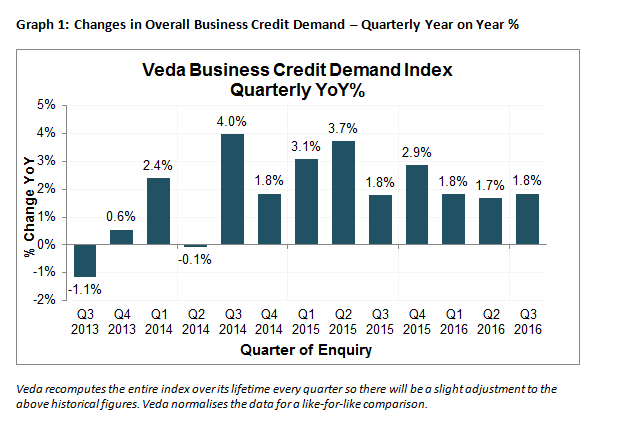

- Overall business credit applications rose 1.8% (vs September quarter 2015)

- Growth in business loan applications rose +3.1% but asset finance rate of growth eased to +2.3% (vs September quarter 2015)

- Trade credit applications remained flat (vs September quarter 2015)

Sydney, Australia – Wednesday, 12 October 2016: The Veda Quarterly Business Credit Demand Index – measuring applications for business loans, trade credit and asset finance – rose at an annual rate of +1.8% in the September 2016 quarter.

The rate of growth in business credit demand suggests any post-election optimism felt in the business community was short-lived.

Neil Shilbury, Veda General Manager, Commercial Risk, said the uptick in business credit demand usually experienced in a post-election quarter had not fully eventuated in this case.

“In most election years, we see a significant boost in business credit demand shortly after a newly elected government has been established,” Mr Shilbury said.

“The September quarter seemed to be following this trend at first, starting strongly in the immediate wake of the federal election. However, the boost was short-lived and demand eased throughout August and September,” Mr Shilbury added.

Business loan application growth (+3.1%) drove the outcome of the Index, released today by Veda, Australia and New Zealand’s leading provider of consumer and commercial data and insights and a wholly-owned subsidiary of Equifax. Asset finance applications were also positive, but the growth rate slowed to 2.3%, from a rate of 6.7% in the same period the previous year.

Although the volume of trade credit applications was flat in the September quarter, this outcome actually represented an improvement after a sustained period of weakness.

The Veda Business Credit Demand Index has historically proven to be a lead indicator of how the overall economy is performing. The behaviour seen in the annual rate of growth in business credit applications, illustrated by Veda’s data, suggests a steady economic outlook.

Business loan application growth was the strongest performer in the September quarter. The increase was driven primarily by the considerable boost in mortgage applications, which rose 14.8% compared to the same period in 2015.

“The jump in mortgage application numbers this quarter suggests a return to confidence around investment in property, by both local and foreign investors,” Mr Shilbury said.

The latest credit data showed continued disparity in business credit demand between the mining jurisdictions (-0.7%) and non-mining jurisdictions (+3.0%). There were, however, early signs of recovery among the mining states, with Queensland leading the way. This positive activity suggests the worst of the post-mining downturn may have passed.

Growth in overall business credit applications was steady in the September quarter (+1.8%). Demand for business credit was once again strongest in the ACT (+12.2%), followed by Tasmania (+4.0%), Victoria (+3.6%), and NSW (+2.7%). Growth rate in the key mining jurisdiction of Queensland (+0.3%) reflected an improved business environment. However, WA (-2.1%), the NT (-7.8%) and SA (-1.0%) continued to show a decline in business credit applications.

Business loan application growth lifted in the September quarter (+3.1%). Of the non-mining jurisdictions, the strongest growth by a significant margin was seen in the ACT (+15.1%). Tasmania (+5.5%), Victoria (+5.0%) and NSW (+4.8%) all experienced growth, while SA (-3.2%) recorded a fall. As expected, the mining jurisdictions were weaker than the non-mining jurisdictions. Queensland (+0.6%) was the strongest performer, trailed by WA (-0.3%) and the NT (-11.8%), which both showed falls.

Within business loans, growth in lending proposals (+5.3%) eased again, while mortgage applications (+14.8%) picked up strongly, and overdrafts (+1.2%) also increased.

Trade credit applications were flat in the September quarter (+0.0%). Growth in trade credit applications was recorded in the ACT (+10.4%), Tasmania (+3.4%), NSW (+1.4%), and Victoria (+0.9%). Queensland (-0.5%), SA (-2.4%), WA (-4.7%), and the NT (-6.0%) showed falls in trade credit applications.

Growth in asset finance applications eased slightly in the September quarter (+2.3%). Across the non-mining jurisdictions, growth in asset finance applications was strongest in the ACT (+9.3%), followed by Victoria (+4.6%), SA (+4.6%), Tasmania (+2.2%), and NSW (+1.4%). In the mining jurisdictions, Queensland (+1.1%) showed the strongest demand for asset finance, while applications fell in both WA (-0.3%) and the NT (-4.1%).

“Queensland’s strong performance across the board, compared to the other mining jurisdictions, indicates the state is emerging from the post-mining boom downturn. In particular, we have seen a notable return to investment in asset finance in Queensland,” Mr Shilbury said.

Applications for hire purchase (-15.9%) fell again in the September quarter, and continued to weigh heavily on the overall result for asset finance applications. Growth for commercial rental (+7.1%) and motor vehicle loans (+11.4%) eased this quarter, while bill of sale (+25.8%) and leasing (+12.5%) applications increased.

NOTE TO EDITORS

The Veda Quarterly Business Credit Demand Index measures the volume of credit applications that go through the Veda Commercial Bureau by credit providers such as financial institutions and major corporations in Australia. Based on this it is a good measure of intentions to acquire credit by businesses. This differs to other market measures published by the RBA/ABS, which measure new and cumulative dollar amounts that are actually approved by financial institutions.

DISCLAIMER

Purpose of Veda media releases:

Veda Indices releases are intended as a contemporary contribution to data and commentary in relation to credit activity in the Australian economy. The information in this release is general in nature, is not intended to provide guidance or commentary as to Veda’s financial position and does not constitute legal, accounting or other financial advice. To the extent permitted by law, Veda provides no representations, undertakings or warranties concerning the accuracy, completeness or up-to-date nature of the information provided, and specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.