Sydney and Melbourne drive lower application Loan-to-Valuation Ratios

The second application Loan-to-Valuation Ratio (LVR) Index, from Equifax and CoreLogic, reveals a continuing downward trend in the national average application LVR.

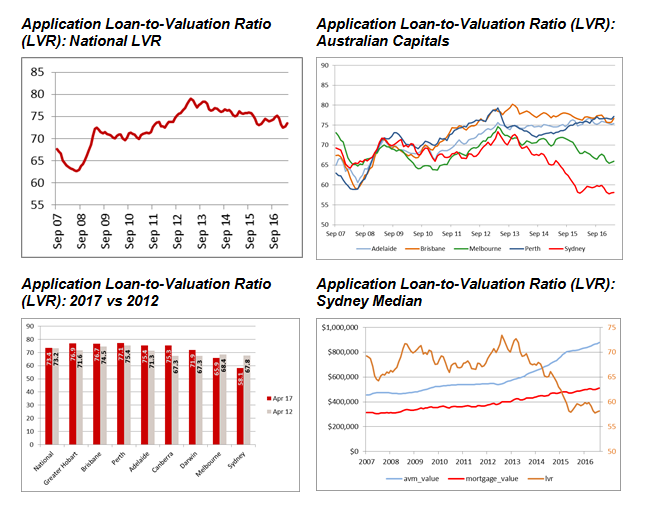

- The national average application LVR has decreased to 73.4% in April 2017, from 74.3% in September 2016

- Strengthening property prices in Sydney and Melbourne have been the key driver of declining national application LVRs (-0.9%), as first home buyers retreat from these markets

- Perth has the highest application LVR (77.1%) and Sydney the lowest (58.1%)

- Mining and agricultural regions are generally exhibiting application LVRs above 80%

SYDNEY, AUSTRALIA, Tuesday, 30 May 2017 – Based on data to the end of April 2017, the national average application Loan-to-Valuation Ratio (LVR) across Australia is currently tracking at 73.4%, a decrease of almost one basis point, since the first Index (released in November 2016). This continues a downward national trend in LVR that began in early 2013.

The Index measures median dwelling values from property data analytics experts, CoreLogic, compared against median residential loan application data from Equifax, the global information solutions company and the leading provider of credit information and analysis in Australia and New Zealand.

The downward trend is in line with APRA statistics that also show a trend towards a higher proportion of mortgage originations with an LVR less than 80%. APRA has also called for a greater focus on responsible lending practices and fewer interest-only mortgages, in March this year.

Neil Shilbury, General Manager, Commercial & Property Products at Equifax, said that the trend towards lower application LVRs can be attributed to a number of factors.

“The strongest housing markets, such as Sydney and Melbourne, have been the primary drivers of lower application LVRs. Since 2012, CoreLogic indices show that Sydney and Melbourne dwelling values have increased by 75% and 54% respectively, yet we have seen loan application amounts increase more slowly. This is driving LVRs down,” Mr Shilbury added.

First-home buyers’ impact on LVRs

Lower LVRs in Sydney and Melbourne may also be due to first-home buyers making up a smaller component of the housing market.

“First-home buyers generally have smaller deposits, and their slowdown of activity may be pushing overall application LVRs down,” said Mr Shilbury.

Statistics from the Australian Bureau of Statistics (ABS) show that first-time buyers represent just 8.0% of owner occupier demand in New South Wales and 14.6% in Victoria.

In Western Australia, where first-home buyers make up 21.7% of the market, LVRs are higher. Declining dwelling values in Perth since 2014 (down 6% in the past 12 months) are also contributing to higher LVRs, with Perth application LVRs increasing by +0.5% since the last Index, to 77.1%.

Mixed LVR changes in state capitals

Average application LVRs in the other capital cities show mixed results. LVRs in Brisbane (76.7%) and Darwin (71.9%) decreased, while LVRs in Adelaide (75.4%), Canberra (75.3%) and Hobart (76.9%) have remained stable.

Tim Lawless, Head of Research at CoreLogic Asia Pacific, said the level of application LVR is an indicator of prudent lending standards and financial stability.

“The last few months have seen further rises in mortgage rates and renewed focus on credit policies. Additionally, lenders face higher capital requirements for residential mortgages, particularly those on high loan to valuation ratios. The banking regulator remains focussed on ensuring mortgage lending is responsible, with a new focus on reducing the proportion of mortgages originating on interest only terms. In this context, regulators and policy makers are likely to see lower application LVR as a positive outcome, reflecting a lower risk scenario for borrowers,” Mr Lawless said.

LVRs increase in mining and agricultural regions, but decrease in coastal regions and satellite towns

Regional markets also show a substantial level of variability. Most are averaging application LVRs over 80%, and a substantial number have LVRs of over 90%.

“The majority of areas with very high application LVRs are linked to the resources or agricultural sectors. In these areas, such as Gladstone, Darling Downs and Murrumbidgee, loan application amounts are high, relative to the dwelling prices. Weaker housing market conditions are also a key factor, with many of the mining regions seeing dwelling values fall in excess of 30% since 2013/14,” said Mr Lawless.

“Regional markets with the lowest application LVR tend to be the satellite cities and coastal lifestyle markets. Satellite cities like Wollongong have benefited from a spill over of housing demand, which has pushed up housing values. Many coastal regions have been impacted by equity-rich buyers seeking out holiday homes and retirement options,” Mr Lawless concluded.

Disclaimer

Purpose of Equifax media releases: The information in this release is general in nature, is not intended to provide guidance or commentary as to the financial position of Equifax and does not constitute legal, accounting or other financial advice. To the extent permitted by law, Equifax provides no representations, undertakings or warranties concerning the accuracy, completeness or up-to-date nature of the information provided, and specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

In compiling this publication, CoreLogic has relied upon information supplied by a number of external sources and CoreLogic does not warrant its accuracy or completeness. To the full extent allowed by law CoreLogic excludes all liability for any loss or damage suffered by any person or body corporate arising from or in connection with the supply or use of any part of the information in this publication. CoreLogic recommends that individuals undertake their own research and seek independent financial advice before making any decisions.