Consumer credit demand increases yet consumers remain circumspect

Consumer Credit Demand Index by Equifax (September 2017 Quarter)

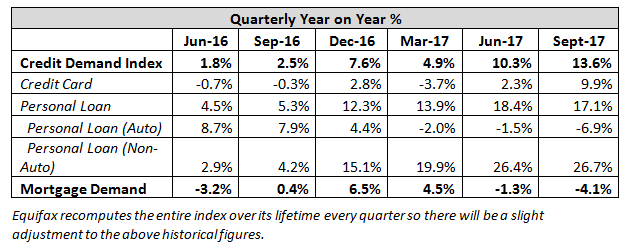

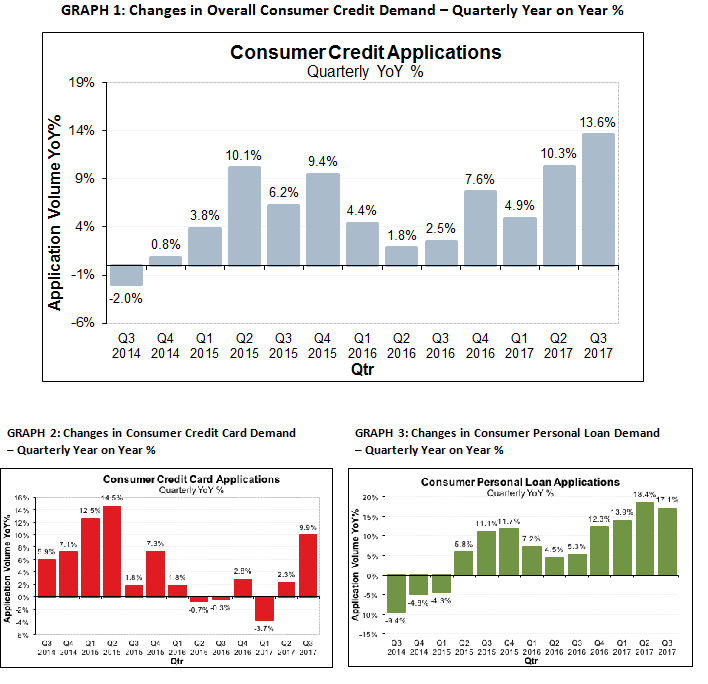

- Overall consumer credit applications rose +13.6% (vs September quarter 2016)

- Credit card applications increased by +9.9% (vs September quarter 2016)

- Personal loan applications also rose, up +17.1% (vs September quarter 2016)

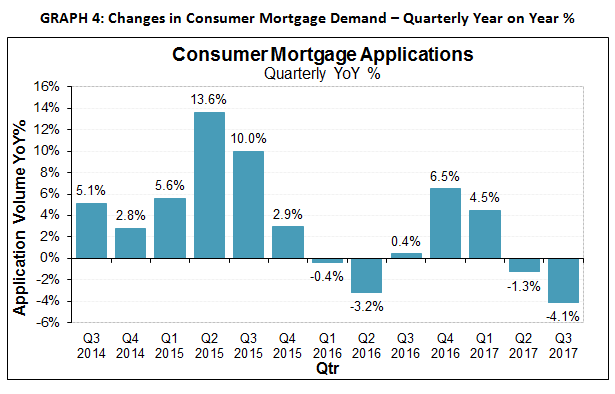

- Mortgage applications declined by -4.1% (vs September quarter 2016)

Sydney, Australia, Friday, 10 November 2017: Consumer credit demand rose 13.6% in the September 2017 quarter, according to data from the latest Quarterly Consumer Credit Demand Index by Equifax.

Released today by Equifax, the global information solutions company and the leading provider of credit information and analysis in Australia and New Zealand, the Index measures the volume of credit card and personal loan applications.

The rise in personal loan (+17.1%) and credit card applications (+9.9%) was in contrast to mortgage applications, which fell -4.1% in the September quarter.

The Quarterly Consumer Credit Demand Index by Equifax provides an early indication of movements in consumer spending and retail sales.

Angus Luffman, Senior GM Consumer Products, Equifax, said, despite the strong credit card and personal loan application figures, the underlying trends indicate consumers remain circumspect.

“For several quarters, we have seen non-traditional lenders becoming more prominent players in the personal loans space, offering new, digital-first products to attract consumers. The rise in personal loan applications in the September quarter is a continuation of this trend,” Mr Luffman said.

“Similarly, the credit card growth is attributable to higher levels of campaign activity from credit providers looking to attract customers away from their competitors, backed by product innovation in the credit card market, rather than being due to consumers taking on additional credit.

“This new product innovation provides consumers more choice, but while they continue to seek the best deals, they remain circumspect about additional exposure to unsecured credit,” Mr Luffman added.

Credit card applications picked up considerably in the September quarter. TAS (+15.7%) experienced the largest increase in application volume, followed by VIC (+12.1%), SA (+10.6%), NSW (+9.6%), and ACT (+9.6%). The NT (+9.0%), WA (+7.9%) and QLD (+7.8%) also showed strong rises in the number of credit card applications.

Personal loan applications continued to experience growth across all states and territories in the September quarter. The strongest growth was seen in QLD (+19.5%), followed by VIC (+18.2%), SA (+17.7%), NSW (+16.8%) and WA (+13.4%). TAS (+11.3%), the ACT (+10.6%) and the NT (+7.7%) showed the weakest outcome, but still recorded solid growth.

Mortgage applications eased again in the September quarter, at an annual rate of -4.1%. Mortgage applications growth remained positive in TAS (+6.6%), the ACT (+5.6%) and VIC (+2.3%), but fell in NSW (-3.6%), SA (-7.1%), QLD (-8.4%), NT (-9.3%), and WA (-19.0%).

Historically, movements in Equifax mortgage application demand data has led movements in house prices by around six to nine months. Mortgage applications are not part of the Consumer Credit Demand Index, but are a good indicator of home buyer demand, and an excellent indicator of housing turnover.

The latest easing in mortgage applications is a continuation in the trend of easing mortgage demand over the past three quarters.

The slowing in mortgage applications has also led to greater activity on the part of the younger demographics, who had their largest increase in share of applications in over three years.

NOTE TO EDITORS

The Quarterly Consumer Credit Demand Index by Equifax measures the volume of credit card and personal loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of media releases from Equifax:The information in this release is general in nature, is not intended to provide guidance or commentary as to the financial position of Equifax and does not constitute legal, accounting or other financial advice. To the extent permitted by law, Equifax provides no representations, undertakings or warranties concerning the accuracy, completeness or up-to-date nature of the information provided, and specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.