Consumers circumspect about credit commitments, despite increased growth in credit demand

Consumer Credit Demand Index by Equifax (June 2017 Quarter)

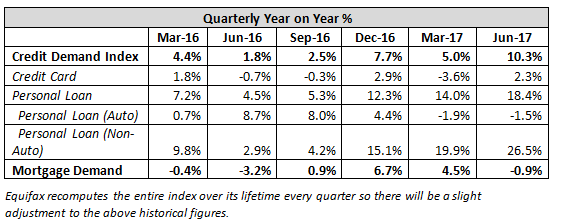

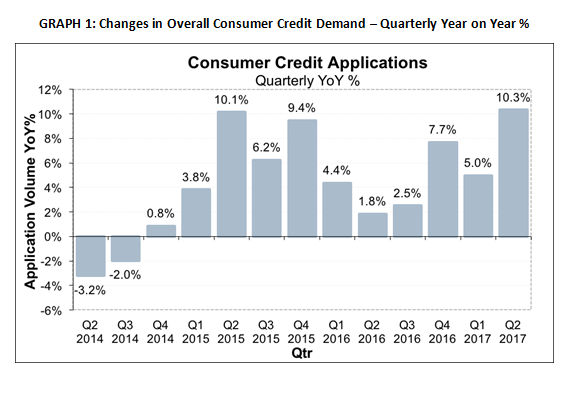

- Overall consumer credit applications rose +10.3% (vs June quarter 2016)

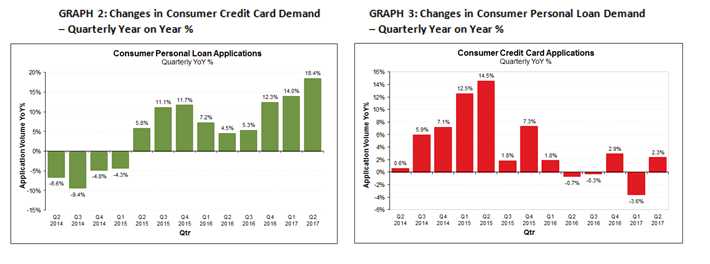

- Credit card applications increased by +2.3% (vs June quarter 2016)

- Personal loan applications also rose, up +18.4% (vs June quarter 2016)

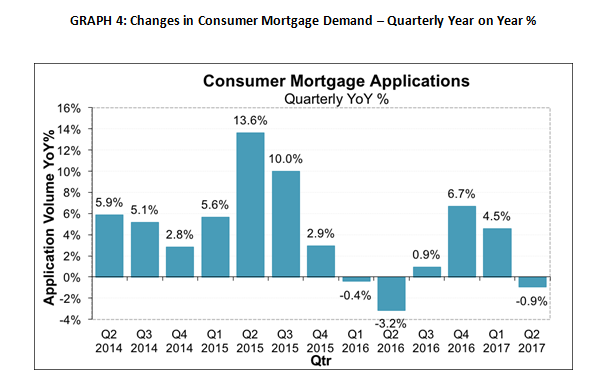

- Mortgage applications declined by -0.9% (vs June quarter 2016)

Sydney, Australia, Wednesday, 19 July 2017: Consumer credit demand rose a significant 10.3% in the June 2017 quarter, driven primarily by a surge in personal loan applications, according to data from the latest Quarterly Consumer Credit Demand Index by Equifax.

Released today by Equifax, the global information solutions company and the leading provider of credit information and analysis in Australia and New Zealand, the Index measures the volume of credit card and personal loan applications.

The pick-up in personal loan applications (+18.4%) was in contrast to credit card applications, which saw an increase of only +2.3% in the June 2017 quarter, and mortgage applications, which fell -0.9% in the same period.

The Quarterly Consumer Credit Demand Index by Equifax provides an early indication of movements in consumer spending and retail sales.

Angus Luffman, Senior GM Consumer Products, Equifax, said the divergent trends seen in personal loan and credit card applications may indicate shifting consumer attitudes toward credit.

“The average value amount a consumer applies for on a credit card has doubled in the past three years. Yet, in the same period, the total credit card balances accruing interest have declined. This suggests consumers are using credit cards more frequently for every day purchases, while also being careful not to add to the debt load,” Mr Luffman said.

“The lift in personal loans indicates consumers are turning to this line of credit as a means to support household and discretionary expenditure. Over the past three years, the number of applications for personal loans at traditional financial institutions such as Credit Unions, local and international banks, has remained stable. In the same period, the number of applications to lenders outside the traditional group has increased 2.5 times.

“Much of this group is made up of recently established lenders with niche offerings, such as alternate payment options in an online, point-of-sale environment.

“Despite the increase in personal loan applications, the total personal credit balances, excluding housing, remain flat, as they have been for a number of years.

“Given the current subdued growth in household incomes, and below-neutral consumer sentiment, it is understandable that Australians may be becoming more circumspect in their use of consumer credit products,” Mr Luffman added.

Credit card applications picked up in all geographies in the June quarter. Tasmania (14.8%) experienced the largest increase in credit card applications, followed by Queensland (+4.5%), SA (+3.1%), the NT (+3.1%), and the ACT (+2.4%). Victoria (+1.9%), NSW (+1.3%) and WA (+0.4%) also showed a rise in the number of credit card applications.

Personal loan applications picked up strongly across most states and territories in the June quarter. Strong growth rates were seen in Victoria (+19.9%), Queensland (+19.6%), NSW (+19.5%), SA (+18.5%), Tasmania (+17.9%), the ACT (+15.4%) and WA (+12.4%). The NT (+4.2%) showed the weakest outcome, but still recorded solid growth.

Mortgage applications eased in all jurisdictions in the June quarter, including in NSW and Victoria where housing markets have been the strongest. Overall mortgage applications fell at an annual rate of -0.9% in the June quarter.

Despite slowing, mortgage applications growth remained positive in Tasmania (+12.1%), and the ACT (+4.9%), as well as Victoria (+2.9%) and NSW (+2.4%). Mortgage applications fell in Queensland (-3.4%), SA (-4.6%), while the NT (-17.7%), and WA (-18.5%) once again saw the most pronounced decline in mortgage demand.

“This is the second consecutive quarter of easing growth in mortgage applications, and the beginning of a downward trend across all states and territories,” said Mr Luffman.

“Any debate about whether the housing market is softening should now be put to rest, as we can clearly see that, even in the historically strong geographies on the Eastern seaboard, mortgage application demand is slowing or already in decline,” Mr Luffman added.

Historically, movements in Equifax mortgage application demand data has led movements in house prices by around six to nine months. Mortgage applications are not part of the Consumer Credit Demand Index, but are a good indicator of home buyer demand, and an excellent indicator of housing turnover.

NOTE TO EDITORS

The Quarterly Consumer Credit Demand Index by Equifax measures the volume of credit card and personal loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of media releases from Equifax:The information in this release is general in nature, is not intended to provide guidance or commentary as to the financial position of Equifax and does not constitute legal, accounting or other financial advice. To the extent permitted by law, Equifax provides no representations, undertakings or warranties concerning the accuracy, completeness or up-to-date nature of the information provided, and specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.