Growth in business credit demand lifts, as conditions and confidence improve

Business Credit Demand Index by Equifax (June 2017 Quarter)

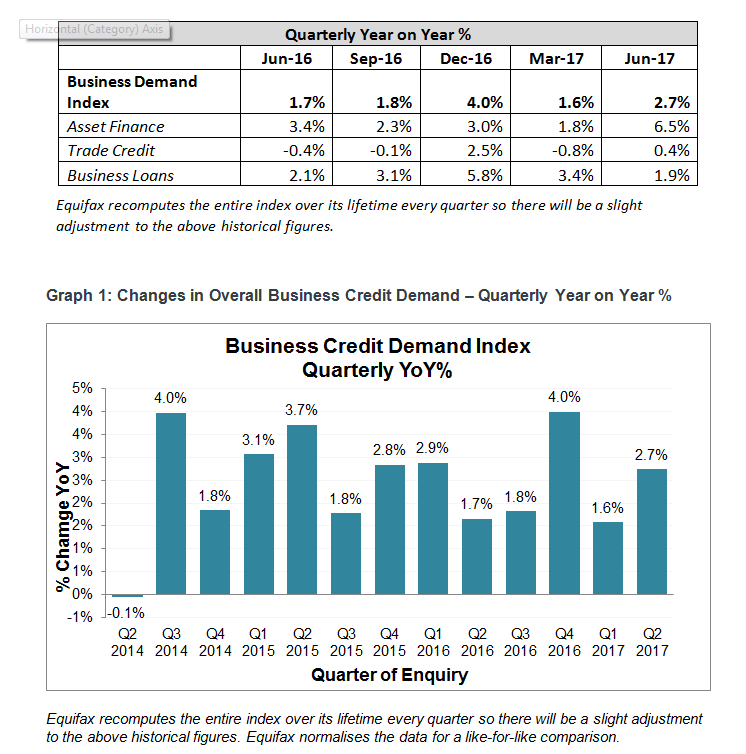

- Overall business credit applications rose +2.7% (vs June quarter 2016)

- Growth in asset finance applications and trade credit applications increased (vs June quarter 2016)

- Growth in business loan applications eased slightly but remained positive (vs June quarter 2016)

Sydney, Australia, Thursday, 31 July 2017 – The Quarterly Business Credit Demand Index by Equifax, which measures the level of business loan, trade credit, and asset finance applications, rose at an annual rate of 2.7% in the June quarter, compared to the same period last year.

Released today by Equifax, the global information solutions company and the leading provider of credit information and analysis in Australia and New Zealand, the Index reflected an increase of +6.5% in asset finance applications, and +0.4% in trade credit applications, compared to the same period in 2016.

The positive outcomes in trade credit and asset finance offset a moderate easing in the rate of growth in business loan applications (+1.9%), which nonetheless remained positive in the June quarter. Within business loans, commercial mortgage applications (+23.1%) continued to show strength, despite also easing slightly in the June quarter.

Neil Shilbury, General Manager, Commercial and Property Products at Equifax, said the growth in the Index signified a positive outlook for businesses; consistent with a number of external indicators.

“The uptick in business credit demand seen in the June Index suggests much of the pain from falling mining investment is passing, helped along by improved conditions in China, which have boosted the Australian economy,” Mr Shilbury said.

“Over the past several months, we have seen stronger company profits, low interest rates, and solid levels of business confidence nationally. In this context, the pick-up in business credit growth seen in the most recent Index is consistent with the better business conditions that have emerged in the first half of 2017,” he added.

Growth in the number of applications for business credit picked up in both the mining and non-mining jurisdictions in the June quarter. Stronger conditions continued to be seen in the non-mining jurisdictions (+3.7%) than in the mining jurisdictions (+0.5%) of Queensland, Western Australia, and the Northern Territory.

Queensland continues to lead the growth in business credit demand in the mining states. The Queensland tourism industry is benefiting from the lower Australian dollar, with international visitor numbers rising, while small business confidence in the state is also recovering.

Growth in overall business credit applications picked up +2.7% in the June quarter versus the same period in 2016. Growth in demand for total business credit was strongest in SA (+7.6%), the ACT (+7.5%), Victoria (+5.5%), Queensland (+2.2%), and NSW (+1.8%). Total business credit applications fell in Tasmania (-4.4%), NT (-3.0%), and WA (-2.8%).

The rate of growth in business loan applications rose moderately in the June quarter (+1.9%). In the non-mining jurisdictions, NSW (+5.1%), Victoria (+5.0%), SA (+3.7%), and the ACT (+1.6%) all experienced growth in business loan applications, while Tasmania (-14.8%) showed a fall. Across the mining jurisdictions, Queensland (-2.8%), WA (-5.9%), and the NT (-20.8%) all saw falls in business loan applications.

Within business loans, mortgage applications (+23.1%) continued to show strength, despite easing slightly from the previous quarter when applications were at +25.7%. Commercial mortgages is a broad category encompassing business investment in new buildings and commercial property for both development and investment purposes.

“While overall growth in business loan applications was moderate this quarter, we are still seeing considerable activity in commercial mortgage applications,” Mr Shilbury said.

“With two interest rate cuts in 2016, lower interest rates may be a key factor in the growth in commercial mortgage applications, as business investment in property remains an attractive prospect,” he continued.

Trade credit applications strengthened in the June quarter (+0.4%). The growth in trade credit applications was strongest in the ACT (+20.9%), followed by the NT (+8.6%), SA (+7.4%), Tasmania (+4.6%), Victoria (+2.8%) and Queensland (+2.6%). Meanwhile, WA (-1.7%) and NSW (-1.4%) both recorded falls.

Within trade credit applications, the main category of 30 day accounts (+3.6%) showed growth, but other account types showed declines, including 7 day accounts (-17.0%).

Growth in asset finance applications picked up in the June quarter (+6.5%). In the non-mining jurisdictions, growth in asset finance applications was strongest in SA (+13.6%) and Victoria (+9.1%), followed by NSW (+3.8%), the ACT (+3.1%), and Tasmania (+1.4%). In the mining jurisdictions, growth in asset finance applications was strongest in Queensland (+8.9%), followed by the NT (+6.3%) and WA (+0.5%).

“The key economies of NSW and Victoria have benefited from favourable shifts in interest and exchange rates,” Mr Shilbury said.

“NSW has a large amount of transport infrastructure work underway, and its commercial construction is healthy. Victoria also has a considerable transport infrastructure spend, and having the strongest population growth in the nation is helping to underpin the state’s broader economic growth,” he added.

By asset finance account type, applications for hire purchase (+2.7%), commercial rental (+5.2%), leasing (+9.1) and auto loans (+10.8%) rose, while bill of sale applications (-8.9%) fell.

NOTE TO EDITORS

The Quarterly Business Credit Demand Index by Equifax Index measures the volume of credit applications that go through the Commercial Bureau by credit providers such as financial institutions and major corporations in Australia. Based on this it is a good measure of intentions to acquire credit by businesses. This differs to other market measures published by the RBA/ABS, which measure new and cumulative dollar amounts that are actually approved by financial institutions.

DISCLAIMER

Purpose of media releases from Equifax: The information in this release is general in nature, is not intended to provide guidance or commentary as to the financial position of Equifax and does not constitute legal, accounting or other financial advice. To the extent permitted by law, Equifax provides no representations, undertakings or warranties concerning the accuracy, completeness or up-to-date nature of the information provided, and specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity