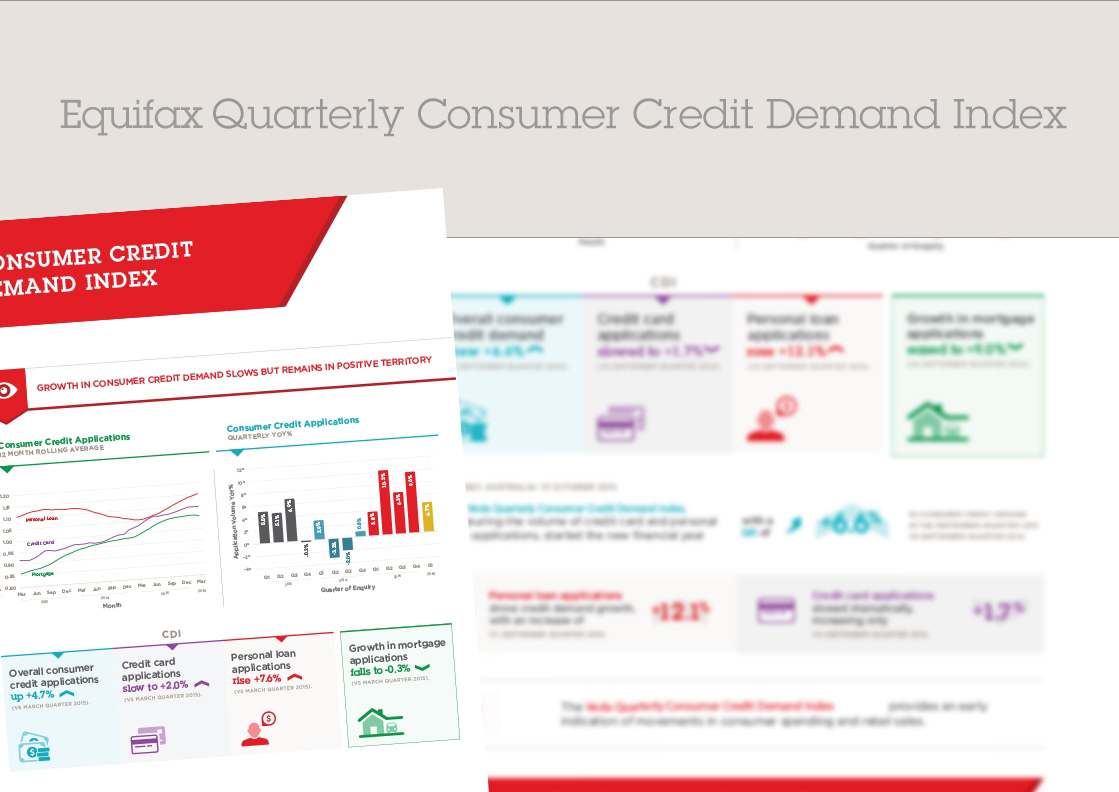

Mortgage demand into double digits, consumer credit relatively flat

Veda Quarterly Business Credit Demand Index: December 2013

Mortgage demand into double digits, consumer credit relatively flat

- Overall consumer credit demand flat at +0.4% year on year

- Credit card enquiries up 2.4% year on year

- Personal loan enquiries down -1.4% year on year

- Mortgage enquiries up +15.3% year on year

Sydney, 21 January 2014: Veda, the data analytics company and leading provider of credit information and analysis in Australia and New Zealand, today revealed the results of its consumer credit demand index for the fourth calendar quarter of 2013. Overall consumer credit demand for the December quarter compared to the same period in 2012 was flat (+0.4%) year on year, representing an easing in the pace of growth from the increase of 7.4% recorded in the September quarter.

The index measures the volume of unsecured and secured credit enquiries that go through the Veda Consumer Credit Bureau by financial services credit providers in Australia.

Mortgage enquiries continued to rise, increasing by 15.3% year on year, an increase from 9.7% in the September quarter and 7.9% in the June quarter.

All states saw year on year growth in the volume of mortgage enquiries in the December quarter. For the second consecutive quarter mortgage enquiries were strongest in NSW (+22.2%) with significant increases also recorded in VIC (+15.2%), QLD (+11.9%) and WA (+11.9%). Other states to experience mortgage enquiry growth were TAS (+9.8%), SA (+8.4%), ACT (+4.8%) and the NT (+2.6%).

“An extended period of low interest rates is supporting the lift in mortgage enquiries, which have stepped up a level and are now showing the strongest growth since late 2009. It is likely that we will see a continuing increase in the near term, along with sustained house price growth. We saw a further shift to mortgage applications from older demographics, with more first home buyers leaving the market,” said Angus Luffman, General Manager of Consumer Risk at Veda.

In contrast, credit card enquiries eased sharply in the December quarter. Nationally, annual growth in credit card enquiries eased to 2.4% in the December quarter, from 13.4% in the September quarter. Reduced demand for credit cards was apparent in all states with VIC (+6.9%) recording the strongest growth, followed by ACT (+6.2%), NT (+3.9%), WA (+2.6%), and NSW (+1.1%). Enquiries were flat in SA (+0.2%) and contracted in QLD (-0.2%) and (-1.0%).

“The December quarter was the second consecutive quarter of growth for credit card enquiries after an extended period of decline. Whilst it was a softer result than the previous quarter, the weeks leading up to Christmas had solid growth and 2013 ended with overall growth in credit card enquiries of 4.3%.”

Nationally, personal loan enquiries recorded a decrease of -1.4% over the year to the December quarter. The NT (+11.0%) was the only state to record year on year growth, with reduced demand apparent in NSW (-0.8%), VIC (-2.0%), QLD (-1.9%), SA (-1.6%), WA (-0.4%), TAS (-7.6%), and the ACT (-2.7%).

“Personal loans enquiries have stabilised at a much higher level after a period of strong growth. This suggests ongoing challenging conditions for retailers of big ticket items and reflects a slowdown of car sales, which have shown no growth year on year, and a reduced demand for larger purchases among consumers in the mining states.

“The December quarter is typically a strong period for credit demand, reflecting the seasonal peak in spending associated with the Christmas period. The relatively weak outcome in loans and credit cards suggests low interest rates are not leading to a significant lift in consumer borrowing as households remain cautious about rising unemployment.”

The most significant change to Australia’s credit reporting system in over 25 years, Comprehensive Credit Reporting, comes into effect on 12 March 2014, bringing Australia into line with other developed economies including the US and UK.

The change to share open credit account and repayment statuses, known as positive information, on credit files will give lenders a more complete picture of a person’s credit history and allow them to make better assessments of credit applicants. For consumers, it means the ability to turn a previously bad credit history into a good one in a much shorter time period and likely benefit from lender product innovation that will come from the ability to better risk rank credit applicants.

"The sharing of positive information is optional for lenders and can commence from 12 March. Whilst it is expected that there will be a period of transition, consumers need to be aware that more information can start to appear on their credit files in 2014”, said Luffman.

NOTE TO EDITORS

The consumer credit demand index measures the volume of unsecured and secured credit enquiries that go through the Veda Consumer Credit Bureau by financial services credit providers in Australia. Credit enquiries represent an intention by consumers to acquire credit and in turn spend; therefore the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER Purpose of Veda Indices releases: Veda Indices releases are intended as a contemporary contribution to data and commentary in relation to credit activity in the Australian economy. The information in this release does not constitute legal, accounting or other professional financial advice. The information may change and Veda does not guarantee its currency, accuracy or completeness, and you should rely on your own analysis and enquiries. Veda has relied on third party information in compiling the Indices and has not been able to independently verify the accuracy of that information. To the extent permitted by law, Veda specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.